Listen Here

In this episode, we had the privilege of hosting Garrett B. Gunderson, a financial expert and founder of Wealth Factory, whose passion lies in dispelling financial myths and helping hardworking business owners achieve prosperity and peace of mind.

In this episode, we had the privilege of hosting Garrett B. Gunderson, a financial expert and founder of Wealth Factory, whose passion lies in dispelling financial myths and helping hardworking business owners achieve prosperity and peace of mind.

Raised in rural Utah with a family history of struggle and resilience, Garrett’s mission is to empower self-made business owners with the financial tools they need to build lasting wealth.

This led to the creation of Wealth Factory, a company committed to helping individuals recover leaking money, connect with financial experts, and establish structures for both immediate wealth and a lasting family legacy.

In our conversation, Garrett shared his remarkable journey from his blue-collar roots in a 4th generation coal mining family to becoming a renowned “financial genius” in entrepreneurial circles. He also touches on the money myths that most people fall into and how a bad financial mindset can affect the way you look at wealth.

Garrett’s dedication to passing on his knowledge and values to his children fuels his drive to innovate new financial tools and technologies that benefit small business owners and entrepreneurs, emphasizing that legacy encompasses more than just wealth—it’s about values and contributions.

Tune in on this enlightening journey to financial empowerment and legacy building with Garrett Gunderson!

In This Episode

- His personal journey from experiencing financial struggles to paving his way to success

- Learning and mastering his path to financial independence

- The importance of financial belief system and money mindset

- Expert tips and insights from the “financial genius”

Garrett, welcome to the show.

Hi Dave, good to be on, I appreciate it.

Awesome to have you on, Garrett. I love connecting with like-minded people. I so much support your mission and trying to break down all of these concepts that we were all taught. We were taught by conventional wisdom, we were taught by schools, our peers, our parents, and all these things.

You’ve pulled back the curtain on what’s happening in the financial industry. You have such a unique background as well, being a financial advisor yourself, and then moving into some of these more advanced strategies. I appreciate your time today. I know the audience is going to jump into this, but for those who aren’t familiar with your background, why don’t we start things there and tell us about your journey?

In June of 1998, I got a life insurance license. Shortly after I got my Series 6 and 63 (Securities Licenses), in 1998 and 1999, I mainly sold Mutual funds and a little bit of variable – whole life insurance. I thought the Stock market was where it was because it was the nineties. The previous eight years were unprecedented. I was young and naive at 19 years old.

Then I had my wake-up call in the year 2000. Most of my clients were my family – my grandparents, my parents, my friends’ parents. They all thought I was smart because I had nothing to do with the market going up. But when the market went down, they were like, “What do we do?” I hated what the firms were telling me. They told them the market’s on sale. I’m like, “That’s bad news for the people who already bought, not good news.” They’re like, “Tell them to earn it for the long haul.” I’m like, “When does the long haul end? When they die?” They’re like, “A dollar cost average.” I’m like, “I don’t know anyone that’s looking to be average”.

Scarcity is the ultimate enemy of wealth.

Fortunately, I had this mentor and he managed five billion dollars in Municipal Bond Fund. He helped me get everybody out of the market between March and May of 2000. Therefore, not losing for the next two and a half years, there were double-digit losses. There were three years in a row of losses. That’s when I decided to focus on what was guaranteed in finance. We’re not even allowed to say that word, but what’s guaranteed in finance is if you could save tax, that’s a guaranteed return.

If you could save interest, that’s a guaranteed return. If you could save non-performing fees and commissions, that’s a guaranteed return. Or if you can remove duplicate coverages or an improper structure with insurance, again, another guaranteed return. I became obsessed with efficiency in helping people keep more of what they make and focusing more on cash flow.

When I was young, I was 19 to 22 years old, I could use being young to speak to people who normally wouldn’t meet with someone. I flew somewhere every single month, 26 straight months, and interviewed the brightest financial minds I could schedule with. I remember being 20 years old, never driving in New York, renting a car, and trying to navigate that chaos, but learning so much because I didn’t know when I’d had this situation where the market went down. I didn’t want to face my clients again and say, “I’m sorry, you’re in it for the long haul.”

I had this red memo pad. I used to take notes and ask because I was curious. That helped me to see the rules that the middle class and the poor were playing, were very different rules from what the ultra-wealthy were playing because I got to see what a Family Office was. I walked into this boardroom, they were talking about a $400 million strategy, and attorneys were questioning how the taxation of it would be and the ownership of it. Investment Advisors and analysts were saying, “What are the risks that are in this?”

The client wasn’t even in the room. I turned to the guy who was presenting at the end. I said, “What is this?” He goes, “Family Office, but it’s a low tier, around 30 to 50 million. You could work with these guys.” I’m like, “I came from a coal mining town. There was nobody worth $30 million or $50 million. No one could have worked for this firm.” I went on this ambitious yet naive process of being, “I need to create this for the average person”.

The more we engage in serving others, solving problems, and delivering value, the more wealth we create.

Like a comprehensive, cohesive communicating team. I realized that’s hard to do because the best people get bought out or gobbled up by these families that have a team that works just for them. Like if someone’s worth $300 million or more, they might have a financial team that is only employed by that family and no one else.

There are these entire networks of Family Office events where they all get together. They’re examining investments and have people presenting investments that aren’t available to the public. It’s like, “This is a whole different world that I didn’t even know anything about.” It opened up my eyes and changed my trajectory.

So many parallels to my story as well, Garrett. It was back in 2000 when I got so fed up with the market and the tech bubble was bursting at the time. I hated that feeling of having no control. You wake up every day and there’s something else in the news. It’s a sea of red, and you have no control.

Then the other thing that I respect about the work that you’re doing in your book, I’ve got a copy of your book right here. We’ll reference this for folks – Killing Sacred Cows. I love how you get into Investor psychology, and think about what is this all about anyway, right? There are tactics, there are strategies that we can employ, and we can follow the ultra-wealthy.

But let’s jump into Investor psychology a little bit because some of the things that you’ve uncovered here are so fascinating. Why don’t we start with an Abundance versus Scarcity mindset?

That’s the first chapter of that book. That chapter is called, The Finite Pie. I remember as you can see by my hair, at one time I wanted to be a rock star. I loved music and I played guitar. My wife bought me Rolling Stone as a subscription. The very first magazine I opened up was a picture of this massive guy. It was a cartoon. He was bigger than all the buildings, eating pie. Little crumbles are coming down with the people below.

The title was The Finite Pie. It was a belief that there’s a win-lose, Zero-sum game that one person having wealth means another person cannot have wealth. That is this foundational philosophy of scarcity. They quoted people in the article, Thomas (Robert) Malthus, who was an economist and said, “We’re going to run out of food.” That was 300 to 400 years ago. I kept thinking, animals have babies and plants have seeds.

Maybe there is a place where there’s too much, but ultimately they were ignoring innovation, ingenuity, and exchange. My belief was in abundance, the wealthier someone is, it means the more value they created, the more other people have been able to receive that value. The more exchange we have through serving others, solving problems, and delivering value, the more wealth is created.

I think we have so much evidence of abundance because there was a time when 59% of the planet, just a few hundred years ago was in poverty. Now it’s 9% of real poverty still exists, but it’s drastically reduced. Even if we look at people that were extraordinarily wealthy hundreds of years ago. I went to the Palace of Versailles a few years ago and it’s a big place, but it didn’t have indoor plumbing when the kings were there.

They couldn’t have whatever food they wanted. It was limited to what was there. They couldn’t get anywhere in the world anytime soon. If they wanted music, they had to bring in a band. Now someone in the middle class has access to even more conveniences through innovation, technology, and value. This notion, if we think it’s all about competition and what we could take versus what we could create, that Zero-sum game mindset harms us, not helps us.

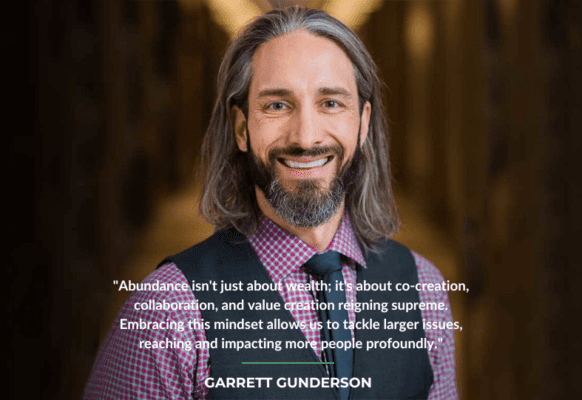

If we don’t conquer the Scarcity mentality, no luck, saving, discipline, ready return or financial person will save someone because scarcity is the greatest destroyer of wealth. It’s a belief system that governs our behaviors, and those behaviors are very limited and they’re very isolated. I believe in abundance, it’s co-creation, collaboration, and value creation that are king. If we can embrace that, then we can be more expansive by solving bigger problems. Serving more people or more deeply impacting the people we serve.

The foundation of everything when it comes to finance is understanding that. If you don’t understand that, then you’re probably going to get persuaded to do things that don’t make logical sense, but someone convinces you of because you believe a faulty premise.

It’s so spot on. In our Holistic Wealth Strategy, that’s phase one as well. It’s all about your mindset and having that abundance mindset, getting rid of those limiting beliefs so you can conquer things. As you said, everyone’s going to come back. You could have the greatest strategies that you share with people, but they’re going to say, “My financial planner said it was too risky”.

Always create a future that’s bigger than your past.

My family and those around me say, “This isn’t for me, it’s too risky.” So you have to have that abundance mindset, to be able to create value and think about the possibilities. Then the second piece to that, I also find fascinating about your journey as well, this concept of never-ending question-asking, and curiosity that you have in life.

That’s part of having a growth mindset. Always creating a future that’s bigger than your past. Talk to us a little bit more about your path of curiosity. Was that the passion or did you have a particular a-ha moment that inspired you on this journey?

My curiosity candidly came from a route of not feeling like I was smart enough early on. When I was a kid, I was in kindergarten. I made this little art project, which was a house out of a milk carton. To get it back, you had to memorize your address. I never did because I forgot to do it. Then finally, on the last day, I gave it a half-assed effort. Everybody in the class got it back, but mine got thrown away.

From the time that I was young, I was like, “I’m stupid.” I did all I could to prove I wasn’t stupid. Great grades, a lot of study, a lot of research, it wasn’t naturally what I would have done. But I had this ambition to prove that I wasn’t dumb and that I wasn’t stupid, which led me to be curious. It served me to a large degree, told it didn’t. Told myself that I wouldn’t speak up until I wouldn’t ask every question because I didn’t want to appear as dumb in a group.

Fortunately, I did work and got over that, but that was my initial thing. My curiosity was I wanted to learn for myself so I could get out of my small coal mining town, move to a big city, and be seen as successful. My definition in my rudimentary mind at the time, is that success is being a multimillionaire. That’s what I thought success was. When I was fifteen, it was probably being a millionaire.

Then I remember getting there at 27 and being like, “It didn’t feel that much different”, and I wasn’t necessarily a whole lot happier. I do think money does directly relate to our happiness when we handle the basics, but once we get past that if we’re not doing things that we enjoy, and we’re not designing a life that we love, and we don’t feel fulfilled in other areas of our life, money as a solo artist can be very misleading.

Where if we’re just trying to build that worth at the expense of our family, our quality of life, our travel, our hobbies. We might check every box society told us mattered and not feel whole. You feel quite hollow, and empty. Wonder why more people aren’t banging down our doors and you’re so amazing. A lot of times our relationship with money is merely a reflection of the relationship we have with ourselves. Anything we haven’t accepted in ourselves that we expect money to fix, unfortunately, isn’t strong enough to fix those things that are more emotional and more wounds that a lot of people have.

If we believe it’s all about competition and taking instead of creating, that zero-sum game mindset harms us rather than helps us.

What’s great is when you can have a whole lot of money, a whole lot of purpose, and a high quality of life instead of a whole lot of money, no purpose, and be exhausted all the time. It’s not that you have to do a way with money to be happy, you can have money and be happy. It’s easier in a lot of cases. It’s that unfortunately, people do things they hate to live a life that they love 30 years from today when they’re so-called “retired”.

But what happens if we create a life we don’t want to retire from? What happens when we become financially independent early and now we can swing for the fences on our purpose and our life design, versus just being in the grind?

That is spot on, Garrett. Many people struggle with that. People don’t spend enough time working on it, especially today. We live in such a reactionary environment. You’ve got many different things coming out at us at the same time. If you don’t spend time to figure that out and get your mindset right, you’re going to plateau, or even worse, the world starts getting smaller without having that right vision for yourself.

Garrett, there are many different strategies and tactics that you uncovered in your book. One of the successful habits I’ve seen with Family Offices and Ultra-high-net-worth (UHNWI) as well, is that they’ve created one kind of overarching framework or overall wealth strategy. Have you defined such a wealth strategy for yourself?

I have a wealth framework for sure. That framework has depth in each piece of the framework, but it begins with simplicity. Financial independence is the first step. Financial freedom is the permanent step. There’s a difference between the two. Financial independence is when we have enough recurring revenue from our assets to cover our expenses.

Whether we show up and do work the next day, we are taken care of. We still have to maintain that by monitoring and managing it. Ultimately, five levers help us create financial independence. Then financial freedom, it’s a perspective or a state of being, where money is no longer the primary reason or excuse we would do or not do something. It’s just not the consideration. When we come from that place, we can make decisions that are based first and foremost on value.

Second on the economic impact or cost and then third on the price. Most people are not financially free to think about the price alone. Therefore, they spend a lot of time trying to save money. We don’t shrink our way to wealth. It’s an expansive game. If I put value first, and economic cost second, which might be, “Maybe I pay a lot more for my financial team, but they provide so much more value than another financial team that would be cheap.”

Sometimes, a high price can be low cost because you’re tapping into the best people and the best resources. In the values, your overall feeling of satisfaction and enjoyment. I want to be financially free at all times, and there’s a framework for that, which is simply how I start my day every day. I start my day with some meditation, with a sauna and cold plunge when I’m home, with some stretching, and then a gratitude journal, and intent for the day. I’m living by design daily.

Financial independence is the first step; financial freedom is the ultimate goal.

A part of how I keep that financial freedom at the forefront is those habits and rituals. When it comes to financial independence, it’s about these five levers. The first one is to plug financial leaks. I’m always looking at efficiency. “Can I pay less to the IRS to interest, on Investment costs, or insurance costs? Is there a way to do that more efficiently?”

Number two, engineering the wealth. “What is the amount of money that has to come in every month to cover my basic lifestyle, and reverse engineering to get there that is first on the foundational pieces, so no money is leaking through like the first step?” Second, the sustainability because we’re looking at mitigating risk in a long-term way, which could be everything from asset protection to education. Then the third piece is an Investor DNA. “I want to invest in things that are aligned with my values, my competencies, my drivers, and I focus instead of diversify.” Focus on creating cash flow.

The third step is accelerating investment income. I look at all my assets and say, “Can I create cash flow?” I look at assets differently than most people. I don’t look at assets as things I have no control over. I look at them as either businesses, real estate, or intellectual property. I’m saying, “Which of those am I going to develop most of my accelerated wealth with?”

Then the fourth step is, that I’m always looking to scale that revenue. If I have control over the outcome of the income with those assets, I can make tweaks by marketing, hiring, developing, and eliminating. That can grow a lot faster than a Blue Chip stock could ever grow. Then the fifth thing is to make it count. I treat myself as my greatest asset. I’m always investing in myself, and I’m always asking, “What’s the highest quality of life along the way that I do not want to retire from my life.”

Plug financial leaks, engineer wealth, accelerate investment income, strategically grow revenue or scale revenue, and then make it count. That’s the framework of wealth for me because it creates that cash flow. Then I have a choice where I could swing for the fences in everything that I do. I have different pieces of that framework where I capture the savings. I like to put it in overfunded whole life cash value insurance as a savings account because I think that’s better than a savings account that’s taxable and doesn’t have a debt benefit with it.

It’s all about your mindset. Embrace an abundance mindset and eliminate limiting beliefs to conquer anything.

That isn’t protected from liability where a lot of people keep that money in bonds, which right now Interest Rates have been going up, lowering those values. They don’t have a debt benefit, so they have to buy term insurance. I don’t have to buy that. I use this cash value as a way to capitalize when economies are chaotic. When the market’s down, my cash value stays strong. I could then buy. When the market’s down, whether that’s real estate, whether it’s acquiring a business, or whether it’s developing intellectual property. People pay attention to me more in down markets with my financial advice.

My books tend to sell more during that time, my courses tend to sell more. When people are lulled to sleep because they’ve had a strong market for no reason other than people that they’re just putting money in, or maybe it’s even fabricated through hedge funds or whatever it might be, they’re not paying attention. But when COVID hits or when the market starts to decrease and when all of a sudden the money they’re putting in isn’t getting them what they want, they start going, “What can I do?”

I’m always looking for liquidity that I can then take as an opportunity where other people don’t have liquidity and profit from day one. I call that – making money on the buy versus hoping it’s going to work out 30 years from today. The numbers are in. 95% of people in America are not financially independent at age 65. That’s including if they have Social Security. That includes if they had a pension or if they had a retirement plan like a 401(k) or an IRA. They can’t stop working and cover their basic expenses.

That’s why I want this framework to cover that within ten years so that now, rather than try to save 10% of my income, I can save 100% in building new assets. That’s why I have nine books instead of one because I build more of those assets. That’s an investment for me that I now can invest fully versus trying to save 10% of my income, and then the other 90% to pay bills. My cash flow is paying the bills and frees me up. That’s part of it. There’s more to it, but that’s the basics.

That’s great. It’s one of the questions I love to ask guests is, what is your wealth strategy? Most people think about it in terms one-dimensionally. They say, “We just invest in real estate. This is what we’re doing. This is how we’re building growth.” But the way you articulated that is this 360-degree view that encompasses that freedom portion, which is essentially what we’re all looking for.

If you can realize that earlier in your life, rather than waiting until you’re 65 to achieve it, wow! Life can be so much more exciting. To that point, you talked about the difference between financial independence, and financial freedom. Something I’ve found interesting is that there’s this FIRE (Financial Independence, Retire Early) community out there. A lot of people want to build passive income in the community, which is great.

Their income will exceed their expenses. But I find in some cases, people are doing that too at fault where they’re keeping their expenses low that they’re not growing. They have achieved that financial independence, but they’re not growing.

Right. There are three ways we can live within our means. A lot of people in the FIRE, they’re like, “Live within your means.” But the problem is they’re only thinking about the first way, cutting expenses. Here’s the thing, there are four types of expenses. The ones that they’re completely spot on with are getting rid of your destructive expenses, overconsumption, borrowing to buy something that you can’t afford, and stuff that you don’t value.

There are a lot of people that are mindlessly letting money leave. The second is lifestyle expenses. They’re minimizing some of the best lifestyle expenses in the name of not having to work. There are certain things that people love. I call it, Mindful cash management is what we want to do. We also want to look and say, “What’s your living wealth account? What if you had some money that you could splurge because maybe you like to buy things that other people think are expensive?”

Hard work within the wrong belief system won’t yield good results.

Maybe this jacket was probably too much for most people. Or maybe a certain restaurant. Maybe you like Michelin-rated restaurants. Or maybe you like to go to the Tour de France. There are all these things, but people go, “I don’t need that.” You might not need it, but you might want it. It’s okay to want it. You just have to manage it and pay cash for those things. But if you get to a miserly mindset, you’re never going to get there.

The third thing is protective expenses. Protective expenses are your asset protection, your estate planning, your corporate structure, your education, and your liquidity. People who are often middle class and don’t know what the wealthy know never take care of these protective expenses and they have to start over more than once through their lifetime. It’s simply because they didn’t understand.

The fourth type of expense is what this movement’s missing, you mentioned the FIRE movement, it’s productive expenses. You put in a dollar, more than a dollar comes back. I don’t budget those expenses. As long as I can manage it and handle it, let’s keep putting money in it because it’s productive. If we get in a mindset that all expenses are bad and we should eliminate them, we eliminate our production. Reduction can help you to get on track, but production accelerates you when you’re on track. Unfortunately, whether it’s Suze Orman, Dave Ramsey, or the FIRE movement, it gets people to focus more on cutting back than creating. The game is a game of value creation when it’s true wealth.

The more people that you can impact, or the more deeply you can impact those people, the more wealth there is because money is a byproduct of value. So the more value you create, the more money you’re going to have. The two other ways to live within your means is to be more efficient, like we said, plugging those four leaks – IRS, interest, investments, or insurance. Then the third one relates to the fourth expense, expand your means.

Why not expand your means? I get that far too often people think materialism will make them happy and they’re going to be disappointed. This (FIRE) movement is right on that. But why in the world would you retire from value creation? What kind of life is it to be 50 years old and have no purpose other than to get up and minimize your expenses? Is that truly going to bring you happiness? I get it, we could give a bird’s finger to the consumeristic world of corporations trying to get us to overconsume. But that doesn’t mean we should stop serving one another and stop living our purpose. That’s what I’m most concerned about in that movement.

Such good points there. I can relate to many of them. I was raised in a middle-class family as well. I was always taught, that there are starving children in Africa, turning off the lights in every room.

I still can’t help but turn off the lights in every room or get after my kids if they didn’t drink the whole drink. It’s still programmed in me even after all this work. It’s an inheritance that I got.

Exactly. It takes a lot of work. One of the things that I’ve done, speaking to your cold plunge and sauna, I created a goal for myself this year to say, “Can I spend $25,000 on my health with extracurricular things?” Purchasing a cold plunge for $6,000, some people would say, “You’re crazy. You’re buying a tub, just like that?”

The health benefits of that alone are massive. I haven’t had a sick day and I can’t even remember when. Reprogramming your mind is so important for some of these things.

Money can contribute to our happiness by covering the basics, but beyond that, if we’re not doing what we enjoy, designing a life we love, and finding fulfillment in other areas, money alone can be very misleading.

You are your best investment. Health is part of that investment. People who don’t take care of their health will later on have to have a much higher price to keep their health. It’s a price I don’t want to pay. I went to my grandma’s funeral earlier this year and a lot of my family members are unhealthy. Surgeries, not doing well. I was extra motivated and it’s cool because my 18 year old is watching that. We work out four days a week together.

He does the cold plunge. He watches Andrew Huberman and does the exact amount he’s told to do. He does the sauna. He hangs from a bar to get his mobility, he gets out and gets some Vitamin D every day. It’s pretty cool to watch him taking care of himself. But that began with me valuing myself, taking care of myself, and having these tools there.

I get some people might be in survival, but part of the reason we get caught in survival is from faulty philosophies where we think hard work solves everything, but hard work with the wrong philosophy still leads to bankruptcy or frustration.

Understanding the frameworks like you’re asking can liberate us from getting past this kind of situation where we’re making an effort but not feeling we’re making progress. I get it, sometimes people don’t have the financial wherewithal today to do what we’re talking about. But if you could look at the things that I’m talking about first thing in the morning, you can write that gratitude and that can start opening things up. You can meditate.

That doesn’t cost anything. You can do the things to invest in yourself without even having to write a cheque or transfer some money. I don’t think people write checks anymore. I don’t think that’s a thing these days, Venmo, whatever these kids are doing. We can invest in ourselves regardless of our financial circumstances.

By watching this, by reading something. By the way, I don’t know if you know, but I have a new book that just came out too. This is my seminal work, Money Unmasked. This is about what the subconscious things, what the relationship to money that we have is just the relationship we have with ourselves. If we expect money to fix our problems, but we haven’t looked at ourselves, it’s not going to help like we want it to and we’ll be upset. We’ll check the boxes, but not fill the fulfillment. There are four money personas that people have.

Once they understand their money persona, it’s more predictable to understand what’s happening. I think of it as not knowing your money persona. It’s like driving around at night with no lights on. You’re going to hit a pothole, you might go off the road. This illuminates it so you’re like, “Now I can see it, and I can make better choices.” That’s what happens when we know our money persona.

For sure. That ties to your Investor DNA that you talked about earlier. Understanding yourself not only the activities and the purpose that you want to do but also investing in those things that align with that DNA that make you happy, they come naturally to you.

One of the things I learned also, what reason I didn’t like the Equity Market is I don’t have a trader mentality. I’m a people person.

I want to be aligned with people that I can make bets on, people I can make assessments on, and are they going to win the game and do that versus just putting my money in some kind of machine and then hoping it is going to turn something.

I can’t imagine sitting there. Because one, options trading is tough because it’s competitive and it’s encyclical. You’re just sitting there clicking a mouse versus talking to a person like you said. Options trading is win-lose. It’s one person who wins, the other person loses. Whether it’s options trading or just trading stocks, I’d rather connect with people. That is disconnected because people start seeing it as a company or numbers on a piece of paper, and it’s not as much about communication and value.

Anything that’s a greater fool theory, one person wins, another person loses, I don’t care whether it can make money, I’m out. You bought my book, Killing Sacred Cows, and I made money from you buying that. I know what’s in the book, so I didn’t need to keep the book. You could be wealthier by reading it and understanding the book. I could be wealthier because you bought it. We both could be better off because we shared and you valued the book more than you valued the 20 bucks, I valued the 20 bucks more than I valued the book. Both parties ended up wealthier in that situation.

The only time that doesn’t happen is when there’s deceit, deception, and over-salesmanship, and I know that gets people jaded. Someone who’s not wealthy could see profit as evidence of deceit, but if someone’s wealthy with ethics, which is more often than not, that wealth is a byproduct of value creation. Profit is evidence of value.

If the mindset of profit is evidence of deception, people will propel and they’ll make sure wealth doesn’t come to them. They don’t want to be bad people. They want money, but they feel like it’s evil. You can see all of those myths harm people where they’re doing their best, but they’re pushing the gas and the brake at the same time and wondering why they’re not getting better gas mileage, why they’re not getting further, and why these other people passing them. It’s our framework. It’s our mindset. It’s our belief system. Hard work in the wrong belief system is not going to equal good results.

For sure. That’s at the heart of capitalism. I always find it fascinating that we have, so many international entrepreneurs in this country because they’ve come where they haven’t had the complacency that we do all of these things that are right at our fingertip. They come to this country, and they have so much gratitude, there’s so much opportunity in front of them. They have that abundance mindset to go and create value.

Which is going to be bigger for communities, having more impact and all those types of things. A lot of Americans sadly look at it, like you said, with that opposite lens which is really self-defeating.

Making money isn’t about having money; it’s about building relationships, delivering value, engaging in exchange, providing service, and being resourceful.

It’s something to be said about someone who walks away from everything and has nothing to lose, they can be a lot more resourceful. Versus someone that’s born on second base and thinks they’ve hit a double, they might not have as much gratitude, might not be as resourceful, or feel like they have too much to lose. In my new book, Money Unmasked, I talk about these two factions. There’s playing not to lose – that’s people holding on to what they’ve got and just hoping that they’re going to make it through.

Then there’s playing to win, which is chasing something at the expense of today. Either way, neither one of them are present. One’s only focused on the past, the other one’s only focused on the future. Neither of them have the joy and fulfillment right now. My argument is, what if you create a game worth winning? What if you set and design a vision that’s compelling that you wouldn’t want to retire from it? Then you’ve actually won, and the win becomes the work that you do, not just the outcomes that you get.

I once heard an interview with Kobe Bryant where he had won five championships, but he said that he had a work ethic because he loved the work, and the win was in the work. Yes, those were outcomes, but he enjoyed it. There’s other people that go, “I’ll be happy when I win the championship”. They win, then what? You said something early on, their future isn’t brighter than their past and they become depressed. When we create a vision, that’s a lifetime vision.

Even when I wrote Money Unmasked, I want to dedicate the next two decades to making this the biggest, most impactful financial book of all time. That gives me 20 years of framework, of working into it, being on podcasts like this, sharing it, living it, and expressing it. When I did Killing Sacred Cows, I wanted to be a New York Times bestseller. Why? Because that was about me.

I wanted to feel validated and sure it was motivating. But once I hit it, I lost steam. I don’t care whether this hits the New York Times or not. I care whether this reaches people’s hearts, whether it impacts their minds. I had someone read it and it was at my cabin on Saturday, and gave me a big hug. He said, “Your words matter to my family. It’s making a difference in how I see the world. Thank you.” That’s a connection.

I love the fact that I can write words and it turns into a cabin that I live in or don’t live in, but go up to. It turns into a relationship I have with a human being. What we don’t realize is when we’re indoctrinated by society of what they think we should do, what they think will make us happy, we give up who we are, and what would fulfill us to appease someone who doesn’t even have our best interest at heart. Napoleon Bonaparte said his life changed the day he found out people would die for a Blue ribbon.

Thinking all expenses are bad and should be eliminated stifles our productivity. While reducing expenses can align us, true acceleration comes from productive investment.

He offered this Blue ribbon, this trophy that people chased. He didn’t have their best interest at heart. He just wanted to win at all costs. When we’re playing someone else’s game that’s not ours, we lose. You know well, as I do, the financial game is rigged out of our favor. It’s rigged against us. When people say high risk equals high return, they want you to take the risk while they get the return. When people say it takes money to make money, it doesn’t take their money, it takes your money.

When people say the long haul, they’re making money on you through that whole long haul. We know that that’s the case. The wealthiest understand that that’s the case, but the average person who says they don’t have the time, money, or ability, just hand their money over to salespeople, hopes for the best, and finds out in the end, that it didn’t end up the way they want it to be. I even wrote a comedy special called The American Ream, using all of my financial knowledge and making it funny. I said, “Everybody’s being sold a dream, it’s actually a ream.”

I talk about everything from Wall Street, Crypto, and Insurance – mainly property and casualty, to taxes and tell jokes around that because I want to reach the people that right now don’t think that they can face their finances. We already know the wealthy are playing by a different set of rules and you’re here to bring those rules to the rest of the world as am I, because it’s really frustrating and unfair to think this is someone’s human life that we’re dealing with. It’s someone’s human capital. It’s someone’s dreams, their daily experiences.

The number one reason listed for divorce is money, but it’s not actually money. It’s when people don’t have their money handled, they stop dreaming. They stop thinking about the future and they just fight over what they have. We’ve got to get it where people can dream again and feel safe enough to be excited, to feel safe enough to feel that it’s possible. But if they’re behind, they have too much Consumer debt, they’ve lost too much money in the stock market.

They’ve done some crazy syndication they didn’t know anything about. When people lose, they lose their life. They lose their joy. They leave bitter and they stop trusting humanity. That’s something that we’ve got to help with because that’s a dark drab place.

What do you think, Garrett, is at the core of this? 98% of the people, they don’t understand even the fact that they are getting reamed at multiple levels. Why do you think that is?

We’re taught to be victims instead of being responsible. We’re taught, “It’s not your fault. You did the best you could. You don’t have the time.” We’re indoctrinated from the time we start that this is how it goes and you got to accept it. There’s $22 trillion in mutual funds. Mutual funds were made so that it was easy and thoughtless. You didn’t have to have a specific amount to buy a share. You could put money in every single month. You could set it and forget it.

You need a framework that transcends scarcity and empowers rather than relinquishes responsibility.

You can invest early, often, and always. Who’s making the most, who are the mutual fund millionaires? The mutual fund billionaires are the people who created them, not the people investing in them. That lie that we’re not capable and that we should trust people who are better at passing tests than us. Let’s say someone goes to an Ivy League school, they’re going to be very intelligent in how to pass the test.

But are they really intelligent in the emotional intelligence and compassion for the person that’s about to allocate their money? Or are they really good at telling a story of why they should be the ones managing it, their firm should be the one managing it, or why they should be in charge? How many of those people from the Ivy League school, after 20 years have beat the Index after fees? They’re really good at telling a story. The problem is that the story doesn’t help us out.

Tell me any Wall Street movie that’s inspiring. Every Wall Street movie is about people being taken. Right? Yet, people do it because it’s complicated. It was designed to be complicated so people don’t question it or think about it. It was designed to say, “This person graduated from this school, so he or she must be smart.” But that doesn’t mean that they’re good at managing your life or your money just because they could beat you in any test that’s in their category.

Fine. That’s kind of communism to a degree, isn’t it? You know better for my life, so you tell me what it is. You promised me I’m going to have housing, but then anyone that’s been to a communistic place, I’ve been in North Vietnam, you see the impacts of communism. I had to talk to people who have been to Cuba. You see the effects of free housing that you have to share with a hundred people because there are not enough people to build it.

There’s no incentive for someone to live their life and add value. It was under the guise of “you have to” because you owe this to someone else. Unfortunately, that’s how we started to treat our money, communistically. “Here, just have my money over.” They promised it’s going to be better in the future and we get there. By the way, they weren’t capable of making it better in the future and you gave up who you were for a false promise. I know that’s hardcore, but that’s what it is.

Our relationship with money often mirrors our relationship with ourselves. If we expect money to fix what we haven’t accepted within ourselves, it won’t heal deeper emotional wounds.

They’re forgetting so many different things. They’re not educating people on taxes, fees, and inflation. Give us, Garrett, in the interest of time here, a couple of your top money myths that you want to share. We talked about a couple of them, but if there’s top two you want to unpack?

You nailed it to start this. Scarcity is the biggest myth. But if we’re talking about money, there are really three that I think go hand in hand and that most people buy into because it’s all this notion of set it and forget it, which is we believe that wealth is a function of how much money we could put away. It takes money to make money. It doesn’t take money to make money. It takes relationships and value. It takes exchange and service. It takes being resourceful.

Money is a by-product of value. Sure, you can make money on your money, but you don’t have to have money to make money. Number two is the second faulty belief is high risk, equals high return. What drunken Wall Street idiot came up with that? Risk means a chance of losing. How does increasing your chance of losing help you win? Instead, I believe in Investor DNA. Mitigating risk and having a team that helps you manage that risk. The more aligned your investment is with you, because the risk isn’t in the investment, it’s in you the investor. If you’re making investments in things you know nothing about, that’s taking risk.

The third one is you’re in it for the long haul. That’s always about compound interest. “After 30 years, you’re finally going to have all this money.” The problem is, what happens in the first 10 years? What happens when life is interrupted, you don’t have your protection in place, the market doesn’t cooperate, or it was more fees than you thought? There’s just too much that people get lulled to sleep in the long haul. People believe wealth is a function of money x rate x time.

High risk, equals high return is the second one. It takes money to make money is the first one, and your long haul is the third one. My belief is, it’s all about velocity. It’s all about cash flow. It’s all about investing in yourself. It’s all about increasing your skill sets so that you can serve more people. Then keep more of what you make with that efficiency, then when you’re in cashflow and you’re economically independent using the frameworks I shared, you’re going to be a whole lot wealthier than putting your money away for 30 years in a retirement plan that’s going to underperform.

Finally, interest rates are doing better now for retirees, but retirees for the last 20 years before 2022 were in trouble because the interest rates were low. Now they’re in trouble because inflation’s so high. Next, they’ll probably be in trouble because taxes will go up and they weren’t trained in that. How insane is it to say, “One day, you’re going to stop working, and then you’re going to create cash flow from your assets. But what I want you to do is never create any cash flow for the next 30 years on your assets.”

Then when you finally stop working, you learn how to make cash flow from your assets. Why not do that over the next 30 years? It’s crazy to me.

You are your greatest investment.

I know, Garrett. That one kills me. We spend our entire career, 40 years, like building this golden goose on this accumulation theory. Then you start to kill your golden goose at 65, and you have this whole fear. I can’t imagine being at this point of saying, are we going to outlive our money?

Scary, right?

It would be scary for a lot of people.

You better not buy that cold plunge. You better start getting high fructose corn syrup.

Exactly. That accumulation theory to me makes absolutely no sense. A lot of people, they’re not asking questions. They’re not being curious enough. Sadly, it becomes too late. You become late in the game, and you haven’t been able to figure that out. So many great points, Garrett.

It is spot on. This is going to help people think through some of these things. If you could give just one piece of advice to listeners about how they could accelerate their wealth journey, what would it be?

I’m going to be the most self-serving guest in history and will say, just buy my book. Buy this right here. Okay, that’s self-serving. But whether it’s this book or something else, you’ve got to get a framework that gets beyond scarcity and that’s empowering versus abdicating responsibility. The number one thing you do is take responsibility. That’s the bottom line. No one’s coming to save you. You’ve got to take responsibility, but if you do, then you can build the right people around you because they’ll understand that type of person.

Profit, when achieved ethically by those not yet wealthy, can be seen as evidence of deceit. However, for those who are already wealthy and ethical, profit is more often a byproduct of value creation. Profit itself is evidence of value.

Awesome. Love it, man. So many great points, Garrett. I appreciate you coming on the show and I look forward to the next chat.

Dave, I really appreciate it. This was fun and I look forward to talking with you again for sure.

Thanks. If people would like to reach out outside of the book, any places, it’s the best links to connect you with?

MoneyUnmasked.com is where you can get the book. If you go to GarrettGunderson.com, you can click on musings, and there’s my blog. Someone said they read all of them, but they’re long. They are long. I write a lot, but I respond to all comments on that. Or if they go to my YouTube channel, which is youtube.com/garrettgundersontv, I respond to all comments that I can make sense of.

Some comments, I don’t know what they’re talking about. Some are viciously mean to me and those I actually enjoy. I do respond in the most snarky smart-ass ways possible. But I do respond to my blog and to my YouTube channel personally.

Perfect. Can we pick up the bits that you have, any of your comedy work? Is that on YouTube?

If they buy the Money Unmasked book, we’re giving them the comedy special that I filmed as one of the bonuses. We’re also giving them the Money Persona quiz, an entire guide, and audio on what their money persona is and how to utilize it to navigate things. That’s the best way.

Awesome. Some great value here and we’ll make sure to link all of that in the show notes for listeners out there. Thanks again for tuning in to everyone. If you’re enjoying the show, please follow and subscribe to the show, and talk to you next week.

Important Links

Connect with Garrett Gunderson

Connect with Pantheon Investments

Books

People

Further Resources

Your 10-Step Actionable Checklist From This Episode

✅ Understand that wealth creation is about value, innovation, and exchange, not competition or a zero-sum game.

✅ Consider the long-term value and economic impact over immediate cost when making financial decisions.

✅ Treat yourself as your greatest asset and invest in personal development, health, and education.

✅ Focus on creating value and serving others to naturally expand your financial means.

✅ Reverse-engineer your financial plan to ensure foundational stability and prevent money leaks.

✅ Identify investments aligned with your values, skills, and interests.

✅ Design a long-term vision that excites you and provides a framework for ongoing fulfillment.

✅ Focus on generating cash flow and economic independence throughout your life.

✅ Recognize that wealth is more about cash flow, value creation, and efficiency.

✅ Utilize educational tools and resources like Garrett Gunderson’s book “Money Unmasked” and other relevant materials.

About Garrett Gunderson

Garrett Gunderson is the author of the New York Times and Wall Street Journal bestseller Killing Sacred Cows: Overcoming the Financial Myths That Are Destroying Your Prosperity. As the Founder and Chief Wealth Architect of the Inc. 500 firm, Wealth Factory, Garrett appeared on ABC’s Good Money, Fox, CNBC, and hundreds of radio shows, and contribute to Forbes. He frequently speak at workshops and conferences and reside in Salt Lake City. Garrett have also been interviewed by renowned figures in personal development, including Hal Elrod, Robert Kiyosaki, Ryan Moran, Dan Sullivan, and Joe Polish.

Garrett Gunderson is the author of the New York Times and Wall Street Journal bestseller Killing Sacred Cows: Overcoming the Financial Myths That Are Destroying Your Prosperity. As the Founder and Chief Wealth Architect of the Inc. 500 firm, Wealth Factory, Garrett appeared on ABC’s Good Money, Fox, CNBC, and hundreds of radio shows, and contribute to Forbes. He frequently speak at workshops and conferences and reside in Salt Lake City. Garrett have also been interviewed by renowned figures in personal development, including Hal Elrod, Robert Kiyosaki, Ryan Moran, Dan Sullivan, and Joe Polish.