Listen Here

![]()

![]()

![]()

In this episode we have Nic Peterson, a dynamic entrepreneur and the co-founder of Mastery Mode. Nic’s impressive portfolio includes co-founding multiple successful companies such as Certainty U, the Certainty App, Relentless Performance, and Relentless Dietetics, now known as Trevor Kashey Nutrition.

In this episode we have Nic Peterson, a dynamic entrepreneur and the co-founder of Mastery Mode. Nic’s impressive portfolio includes co-founding multiple successful companies such as Certainty U, the Certainty App, Relentless Performance, and Relentless Dietetics, now known as Trevor Kashey Nutrition.

With a track record of founding or co-founding over half a dozen companies that have achieved seven or eight-figure revenues, Nic brings a wealth of experience and insights to the table.

Throughout our conversation, Nic shared his journey from experiencing significant successes to enduring challenging failures. His approach is deeply rooted in being a perpetual student, constantly developing new skills and learning from every venture he undertakes.

Nic emphasized the importance of implementing lessons learned, which has been a cornerstone of his growth and success. Nic’s current focus with Mastery Mode is on helping business owners, consultants, and service providers build robust systems and operations.

Tune in to this episode for an engaging and insightful discussion with Nic Peterson, and learn how his strategies can help you achieve your business goals.

In This Episode

- His personal journey of founding multiple companies, detailing the successes he has celebrated and the valuable lessons learned from his failures.

- Important concepts from his book Bumpers: The Framework for Finding Your Personal Abundance, Maximum Productivity, Greatest Profits and Highest Quality of Life.

- How creating efficient systems and robust operations can help business owners, consultants, and service providers leverage their time and increase profitability.

- The significance of continually developing new skills and implementing learned lessons to drive personal and professional growth.

Nic, welcome to the show.

I’m glad to be here. This will be fun.

You bet. Super excited to have you on the show, Nic. I know you’re going to have people think about their thinking by the time they finish this episode and see things in a different light. That was one of the first things when I first heard you talk that I felt was parallel and intriguing.

The way you’re thinking about wealth, the way you’re thinking about value creation, and what’s important because too many people just get caught up in chasing a shiny object or they heard about this investment, they heard about the latest in Crypto from their buddies. So they’ll say, “I got to get in this”. The fear of missing out, and they want to jump into whatever the Asset class is.

It’s all the psychology of it. I read your book, Bumpers, which is a fascinating way to look at it. I know you have a lot of strengths around systematizing businesses as well, and then how that applies to investing and the theory of constraints.

Why don’t we start to unpack some of those and to level set for folks who don’t know who Nic Peterson is, haven’t heard of Wolf Den, or maybe one of your other businesses? You could tell us a bit about how you got here.

That is quite the story. I haven’t practiced. I don’t have the Brendon Burchard trauma story dialed in yet. Right now, I have only a bit of background. I have a portfolio with nine companies in it currently and four of them I own and operate. They’re all different kinds of domains, and different industries.

The way that I ended up getting here is I have an Operating System, which you are familiar with if you read Bumpers like the base of that operating system. I realized years ago, that there’s nothing new under the sun. It’s the same stuff over and over.

I started in fitness, got into exercise with the gym, and then a nutrition company. I had a third business coaching with other people on how to do what we did and that sold for fifty-six million dollars. All of these people came from all these other worlds. I used to have a client as a farmer from North Dakota. He said, “Hey, I have a farm. Can you help me?” I said, “I don’t think so, because I’ve never had a farm.”

As we’re talking, the language is different, but you realize as you have a difference, they are the same patterns, these are the same things. Most of the time, it’s less about knowing the technical details if you talk to investors.

However they invest, whatever the criteria are, whatever the technical details are, people get lost in all that. There’s another side to that, and that’s the human doing the investing. I call it the ‘Adaptive Dilemma’ which you can have all the best theories in the world, but if your Amygdala gets hijacked and you make impulsive decisions, then the plan won’t matter because you’re not following it anyway.

I started developing this in fitness, realizing that people have a plan and then there’s what they do. They’re two different things. They’re most of the time completely unaware of the gap between what they plan to do and what they do. They do whatever they do, they’re not aware of the gap between what they do versus what they’re supposed to do.

Whatever the outcome is, they think that’s a byproduct of the plan. They’re gauging the efficacy of the plan based on the outcome, which is nonsensical because they didn’t do the plan. You only followed it 72%. I was observing that we all engage with business, fitness, investing, and our family, we have these plans and these feedback loops where would say, “I tried this, and this is what happened.” It’s recognizing that you didn’t try ‘this’. “This is what happened, but you didn’t try this”.

We can rewire our brains to appreciate when a bad thing doesn’t happen

You wrote this down and planned on doing this, but you did something different. Until you recognize that your feedback loops, especially in terms of getting what you want, they’re going to be broken. I’ve taken that in fitness and went into business. I started a mastermind, but I didn’t want it. I just had a line of people ready to pay for it.

My rule was this – no two people in the same industry that does the same thing. I didn’t need the money and I got bored easily. I wanted to see how many of these different domains, and how many patterns and principles we can identify that cross over into these other domains. It was thirty-six grand a year. In the first month, I had forty-four people. It’s forty-four people who did forty-four different things.

I did that for two years and I spent all day every day because I was fascinated with everything going on. Identifying these patterns that show up over and over regardless of what domain you’re in, what you’re selling, and what you’re investing in.

Through that, the most interesting are the ones with the most alignment out of those forty-four people, which I started pulling partnerships. That’s where most of my companies come from now. I want as many diverse people as possible to coach them. Then I wound down the coaching and focused on the handful that I think are doing something cool, interesting, and impactful.

That’s what Bumpers, R3, everything that I write about fundamentally. I’m mostly only concerned with the repeating patterns. I don’t get super deep into like, if you’re in medicine, some things apply to medicine and only medicine. It’s not for me. I’m not a doctor. I don’t need to know all that stuff. However, those experts do tend to miss the fundamental recurring patterns. That’s where I am the most helpful or useful to them.

Fascinating. Would you say all those patterns are encapsulated in your book, Bumpers? Would that be the essence of it?

No, but if we talk about the highest return, those are the highest leverage most common. In Bumpers, you have to appreciate, and bad things don’t happen. Race the floor. You can’t win a race you don’t want to be in. Those are the first. If you want to get from A to B, it’s helpful to not get blown up, and step on a landmine. It’s helpful to go in the correct direction.

Those are the two things that you can avoid dying and you’re pointed in the right direction. If you’re the kind of person who’s reading this podcast, then you’re a driven person. Those two things are enough. Just don’t go in the wrong direction, otherwise, you’ll kill yourself.

Why don’t we unpack that more for the readers? If people haven’t read the book yet, let’s get into detail on Bumpers about killing yourself. It’s an interesting concept, but I was also contemplating that as well on some of the other theories that are out there, things like Yin and Yang. There are so many versions of reaching peaks, then you’ve got lows. That’s the kind of life in managing that. Tell us a bit about Bumpers.

I love that you mentioned the yin-yang theory because I have a grandmaster. I have to study all five phases of Yin yang. Bumpers are one of the recurring patterns and I saw this first in fitness and I’m grateful. For a while, I was embarrassed being a fitness professional because they don’t always have the best reputation.

But I’m grateful for everything that I learned in the context of Biology because it’s a complex system. It’s adaptive. If you can learn through the lens of Biology, complex systems start to make more sense. Things like emergent properties, etc.

Watching these gym goers – my clients at first. I’m a resource allocation guy. I learned young, I went pro, and strong man. My coach gave me this whole spiel about how important it is to conserve energy. It stuck with me.

From a resource allocation standpoint, the number of people that do the yo-yo diet; gain 30 pounds, they lose 30 pounds. You see the tremendous amount of resources that go into losing that thirty pounds each time. It’s a significant amount of time, effort, bandwidth, and money. Again, from a Resource allocation standpoint, it was like, “What is going on?”

If you could put all of that effort that you’ve put into losing the same 30 pounds over and over to make progress, you would be so much further along in such a better place. That’s the pattern we kept seeing.

Let’s say you had a million-dollar month, then you had two months where you lost a million dollars, and then you had another million dollars a month. In the first case, if you avoid the weight gain, you can recapture all that time, effort, money, and resources, and put it into inching forward and making progress. So why aren’t you doing that?

My observation and I talk about this quite a bit, if you have a family member who is pre-diabetic and has maybe struggled with their body emission weight for some amount of time and they lose 30 pounds, what happens? They celebrate, you celebrate, everybody celebrates. It’s a massive Dopamine hit. Then let’s say your sister never gained the weight to begin with. Nobody’s celebrating her. There’s no Dopamine for avoiding bad stuff.

What our brains learn over time is if I want a Dopamine hit, I could just dig a hole for myself and dig myself out. Free Dopamine. Whereas making progress, as you know, it’s hard, it’s painful. There’s not a lot of rewards. A lot of people get stuck in this loop.

It’s like the entrepreneur that shows up at the office and starts a bunch of fires so that he/she can put out a bunch of fires and go home feeling like they’re a superhero firefighter. I see this pattern over and over, which is why I wrote Bumpers. I understand why we celebrate getting out of a bad situation, but that’s still not ideal because you were in a bad situation – you lost time, money, and all that stuff damaged relationships.

Can we celebrate or rewire our brains to at least appreciate when a bad thing doesn’t happen? We had people come in for coaching and the mastermind. They would start making progress in leaps and bounds. That’s why we had so many people come in through referral and would say, “What’s the magic?”, “What is Nic doing?”, “What secret tip or trick does he know that nobody else knows?” I’ll just say, “Here’s what we do: we go back, we identify all the bad things that happened, then we figure out how to avoid them in the future.” That’s the secret sauce.

Bumpers is foundational. You know how many entrepreneurs, how many people in general – investors; they’re looking at Crypto, they’re looking at AI (Artificial Intelligence), they’re looking at high upside assets because on some level they’re trying to push harder on the gas. They’re trying to get to wherever they’re going faster. I get it, but maybe we should take our foot off the brake first.

That’s what Bumpers is. Just take the break off, then push on the gas. It gets more surprising to me, I wrote it six years ago, and it gets more and more popular. Hopefully, people are starting to appreciate or at least think about avoiding bad things.

I love that, Nic. I recognize that pattern in investing. That’s when in 2000, I took a complete bloodbath when the tech bubble happened. The market blew up, and I was in the tech industry so I was heavily invested in it. I believed in it. I recognize this pattern that a lot of people don’t see on the equity side of the equation, which is that one of the biggest wealth destroyers is Stock Market losses over time.

People often get lost in the technical details and criteria of investing, but there’s another side to consider: the human doing the investing.

Everyone thinks about, “Last year it was 15%. It was great. A year before, it was 18% and we were up 12%, we’re doing great. I got that statement and everything is good.” But they forgot that in 2008, when the market was down 30%, that takes your compounded number of where you were brings it all the way down.

What you have to do to even get back to where you were takes an enormous effort. That ties exactly to your metaphor of losing weight. It’s the same thing with investing. It’s all the Psychology of it, but people lose it every time, which is in investing.

It’s the same stuff over and over. The interesting thing about investing from my perspective, I deal with quite a few investors. These are very intelligent people, who struggle with this concept, which is risks and probabilities. There are no certainties. In my mind, it’s always risks and probabilities. That’s what we’re processing when we’re investing.

“I got 18%”, does that fund your life goals? No. Well, it doesn’t matter, because the purpose of all of this is to fund something, I assume. There’s this concept, this is our operating methodology; we figure out what we’re trying to fund and in what timeline we want to fund it, such as turning a multivariable equation.

Investing came up; this is how we think about appreciating when bad things don’t happen in regard to investing. I’ll give you an example: somebody said, “Where should I put my money? We just saved our one hundred and thirty grand a year. Just going through recapture, reallocate”. She’s done really well.

I said, “What’s the most important thing to you? Because all I care about is you get what you want. I don’t care about anything else.” She said, “The most important thing is my son going to college in four years. I want him to go to Switzerland. I want to be able to pay for it and I would love to stay with him.” She doesn’t care how much that can cost. She said, “I need an extra $400,000 above what I have in the account for that now.”

I said, “Cool. We just saved you $130,000 a year. Over four years, you’re already there. You just take that money, you save, and put it in the account. The most important thing is you locked in a hundred percent Probability, and it’s all probabilities.” She agreed.

Five minutes later she said, “Where should I put that money?” I said, “In the bank account is where you should put that money because it represents something important to you.” She said, “I think about Real Estate. What do you think about that? What is the probability?” I said, “If you take that 400 grand extra and put it in Real estate, the probability that you get what you want has gone down. That Real Estate might 10X in ten years.”

That’s tempting because it’s more, it’s bigger, it’s opportunity. However, the probability that she get all of that money out in profit in four years is relatively low. She’s putting the important thing at risk by trying to make more. That’s the kind of how we appreciate when bad things don’t happen. What’s the most important thing? ‘This’. Then, fund it as soon as possible.

If you want to fund it in two years, don’t put that money somewhere that’s going to take more than two years to mature because it might be more, but you’ve decreased the probability that you get what you want. That’s the game of – how do we appreciate when bad things don’t happen? Don’t do things that lower the probability that you get what you want.

That is spot on, Nic. In my book, The Holistic Wealth Strategy, that’s exactly what we talk about, which is creating that vision for yourself first before you look at any investing, no matter what your numbers are. It’s getting crystal clarity on your freedom of purpose, freedom of time, freedom of money, and what is it you’re looking to do because everyone’s got something different for them.

I love how you frame that in terms of certainty and probability. Do you have some type of model that breaks that down further about the kind of an Asset Allocation Model or something to morph that too?

Don’t do things that lower the probability of achieving what you want.

We do. I’ll do my best to explain it. Even separately, I can shoot a Loom video or show you the tools. It starts with what we used to call the ‘Solvable problem’. They still call it a solvable problem, but I sold that company and it’s trademarked so I don’t use it anymore. It’s about getting clear on what’s your number one priority.

If your number one priority is to pay off your mortgage, and you want that done, that’s the most important thing for you, cool. How much is that? What timeline? Now we have this problem that we can solve. Here’s the high-level overview – where you’re at, and where you want to be. We only deal with one priority at a time. I’ll explain why this is just my preference. Just a disclaimer, I’m not a financial advisor.

I fund one priority at a time in the order that I prioritize it because if you have three priorities you’ll say, “I’m going to put a third of my money here, and a third of money there. In nine years, I’ll fund everything.”

In a vacuum, that might work. However, let’s say four years or three years in, Covid hits. Now you’re up to creep without a paddle and you have things partially funded with no path forward. Had we funded entirely the number one priority and then Covid hit, you’re up to creep without a paddle, but at least you got the most important thing to you. We waterfall.

The way we do that is, the number one priority is X. Like, your brain says you can have it all, but let’s assume that time is going to pass and randomness exists. If you could only have one, what would the most important thing be? Boom, then that’s number one. That’s always hard because nobody ever wants to admit what the most important thing is. Whole different story.

Then we say, “Given where you’re at, and what you make.” This is where we flipped the Math on its head. If they’ll say, “I want to be here in four years. That’s my number one priority. Given where I’m at today, I need 11 percent a year.” That tells me the kind of risk profile that you should be playing with.

If you need 11 percent a year you’ll say, “I’m going to go to Crypto.” I’m going to say, “You don’t need to take that kind of risk to get 11% a year.” If you need 3% a year with cool bonds, I’d probably get that in the SMP. Let’s say I go into an investment that I think will get 11% a year, and it overperforms and it does 17% in the first year.

You can have all the best theories in the world, but if your amygdala gets hijacked and you make impulsive decisions, then the plan won’t matter because you’re not following it anyway.

We would take that 6% overage and either take it off the table or flip it into something less volatile, and less risky, which is hard because everybody wants as much as possible. But we’re saying, “No, take the overage, take the overperformance, because we’re playing the game of increasing probability. We’re not playing the game of as much as possible.” Then you do the same thing.

If you’ll say that this is your number one priority. I’ll say, “You’re going to need 37% a year to fund that.” Can we increase your income? Can we find another way to make that number smaller? But let’s say you need 37% a year, you’re going to have to play, you’re going to have to take more risks. I don’t consider it risky because the biggest risk is if you need 37% and you put your money into something, that’s going to get eight, you are guaranteeing that you don’t get what you want. You’ve driven the probability down to zero.

The way that we process risk, depends on what you need to get what you want. If you need 37% and all your money is sitting in something that gets you 6%, that’s the riskiest thing you could do. You’re just guaranteeing you don’t get the most important thing to you, which doesn’t make sense to me.

The kind of our model is, can we figure out what kind of return we need to lock in the most important thing? That will inform us to some extent – the timeline. It informs us what options we have. If you need 7%, you have all kinds of options. If you need 2%, then I would wipe most of those options off the table because they’re too risky. If you need 45%, you wipe all the safe stuff off because you have to get 45%.

We do take the overage. There are three things that we do with overage. I’m very simple, I’m not a complex guy. Take it off the table, and put it under your pillow if you want. Flip it into something less risky Bonds. Or if you want to collapse the time down, you could take your big bets with that 6% overage to house money.

Do that with priority. Once the priority is funded, roll it down to the second, and the third, and systematically try to lock in the things that are the most important to you with the appropriate amount of risk, which is relative to where you’re at and what’s important to you.

It’s such a top-down approach. That’s very strategically thought out, but the majority of investors come bottom up because they’re just looking at the specific investment themselves. They’ll say, “I’ve got to be in this” or “I’ve got to be on that” because of whatever’s driving them or to your point about what the amygdala saying, “I just need more.” That one sounds better.

But, this is so purpose-based. We think about that from an Asset allocation model and talking to a lot of Family Offices, and everything. We think of it as a pyramid. In the pyramid at the base level, you have your lowest amount of risk and you have the most amount of certainty.

As you move to the top of that pyramid, you’ve got your highest amount of risk. It’s speculation. That’s where I see some of the Crypto sitting up there. Whether it’s much higher returns, businesses even, or Angel investing. You have no control over that. Let me ask you, Nic. What is your Kolbe score? Do you know your Kolbe score off the top of your head?

We’re playing the game of increasing probability, not the game of maximizing every possibility.

It’s funny because Justin Breen, I don’t know if you know him.

I do.

He’s at my office right now. He’s upstairs and he’s a freak about Kolbe scores. I’ve sent him mine. I don’t remember the order. I am an eight Quick Start, a seven Implementer, then Follow-thru, and Fact Finder are low.

Interesting. I would have guessed that you were a long Follow-thru because of the way you’re systematizing your businesses and the way you’ve picked up on all these patterns. I’m a seven Follow-thru. If any of the listeners haven’t done that, I recommend taking this.

Go to Kolbe.com. It’s a 20-minute test and it unpacks your instinctive nature, on how you’re wired. This applies to investing, entrepreneurship, you name it – so much. I was in the tech industry doing a lot of process consulting.

To me, understanding this and knowing that I’m a systematized thinker, really explains exactly why I’ve been trying to systematize wealth building for so long, to your point. It’s a process. If you get on the scale, you’re trying to lose weight, and you’re chasing that number, it’s completely volatile. But if you focus on the process, then you have your purpose aligned, and as you pointed out, you’re much more likely to achieve the results.

I agree. I tell people this all the time – I will appear if you follow me around day to day, I do look like I have high Follow-thru, but it’s because I know that I don’t. That engineer systems and I’m an Implementer. I got to touch the stuff. I engineer systems to put problems in front of me and I can’t help but do something about it.

I engineer Follow-thru by making it like I piggyback off my quick-start nature. It’s like the same stuff, but it feels that I built a system where it shows up to me randomly and I am like, “I got to fix this.” It looks like a high Follow-thru that’s why I have to system my stuff that way. Otherwise, it’ll never get done.

Are any other systems or patterns that you’ve recognized from your businesses that you’re applying to your investing now?

The biggest one, I built my whole portfolio this way. You can learn more about it from Nassim Taleb in Antifragile, in all of his books. I don’t know if he talks about that in The Black Swan, but it’s the concept of, he calls it the ‘Barbell (Strategy)’. It’s a bimodal strategy.

It’s Seneca’s bimodal Risk Mitigation Strategy, which is on one side, you’re extremely high upside investments or activities. On the other side, you have your reliable ones. People always, especially in the entrepreneur world, confuse the Barbell all the time. I did not say passive, I said reliable and they are different things.

Everybody goes for passive. You’re upside stuff, you’re reliable. It could be passive or active in either scenario. What I’m looking for is things that have a tremendous amount of upside. The mere fact that they have so much upside, we know they’re not reliable, then you have reliable on the other side.

In a business context, a lot of people start a business because they think that it has infinite upside and they learn quickly, but it doesn’t. Such as an Accounting firm, it is a relational business, it doesn’t have the scale that everybody thinks it has. It’s not an upside play and it’s not reliable in the sense that, “Could you tell me exactly next week, how many hours are you going to be in the office? What are you going to do? What’s the outcome going to be?” I don’t know. I just show up.

It’s not reliable. It’s not going to function without you. Even with you, it’s variable. The outcome is all over the map. It’s a smack dab in the middle of the Barbell, which means it doesn’t have an upside, nor is it reliable. It’s a job. I don’t want to be in the middle of the Barbell ever.

Our human instinct, pulls us to the middle because the upside stuff, we want more certainty. We try to pull it toward the middle and the reliable stuff, we want to be exciting, so we keep breaking it and it goes to the middle.

Our human instinct keeps pulling everything to the middle and I’m actively pushing everything out. It’s either an upside play or it’s a reliable play. In our businesses, it’s like, “These are Liquidation plays and these are Cash Flowing plays.” If it sits in the middle, it’s neither. It’s not a reliable cash flow. It doesn’t have an upside. Therefore, it should not exist.

Investing – I look at it the same way. I built my portfolio based on our investing strategy. A handful of my companies are specifically, I don’t care about the enterprise value because the role that they fill is reliable cash flow. With other companies, I don’t care about the cash flow, because the role that they fill is a massive exit later.

Investing is the same kind of back to, let’s say we need 11% to reach all of our goals. What I would do is, I would try to have things on the reliable side that have an expected value of greater than 11%. That overage, if it were me, I would flip it over into investments on the other side with tremendous exit capacity. Because of probabilities and risks, if I say, “I want to get from A to B in six years,” and if I get 11%, I’ll do that.

I want this robust because I want certainty that in six years, I’m going to get everything I want worst-case scenario. If there’s overperformance, or I get a Tax Return, or I get anything above that, I’m going to put it on this side of the barbell. On one hand, one side of the barbell gives me certainty. That I’m going to get what I want.

The other side allows randomness to potentially collapse that time down from six years to three years. One big exit and boom, you’re there. That’s how I build everything. For an investment strategy, I want the reliable side to fund everything important to me in a timeline that is fair and appropriate. Worst-case scenario, if I get all of this stuff in ten years, it’s fine. It’s not ideal, but it’s fine.

I let the randomness of the high upside. Crypto falls in the high upside stuff. Bitcoin goes to a million bucks. Sweet. I reached all my goals faster than I expected. Even if that didn’t happen, I locked it in through the reliable side. That is a bimodal strategy. I fight like hell to stay out of the middle. If it doesn’t have a massive upside, it’s not super reliable, then it doesn’t have space in my Investment Portfolio.

That’s such a great way to think about it. Create that certainty because I think about the psychology of why are you investing. People don’t ask, “What is this going to do for me?” Ask why until you can’t ask why anymore to keep drilling down.

Oftentimes, what you’ll find is, to your point, it’s trying to create certainty out of something because they’re in a job that might go away. Or maybe you’re having a child come on the way and you’d like your wife to stay home with the child or one of the parents. You’re trying to gun for that.

Creating the certainty to do that gets you there. Then you get to pick your investment vehicles and Asset classes that will support that. Tell us a little bit about it from a Crypto perspective. We don’t need to get too deep in the weeds on this.

We do have a ton of tech investors and entrepreneurs in the community, so everyone has good base knowledge. Just give us a little bit about the state of the market in Crypto, as to where you’re seeing it trend right now.

You got Crypto. I know a lot of people who invest a lot of money into Blockchain, but they’re not buying Cryptocurrencies. There’s that distinction which is, there’s the Blockchain – which is the underlying tech that stores data in blocks instead of columns and rows. Then you have the assets that live on the blockchain and are transferred on the Blockchain, the Cryptocurrencies, and the NFTs (Non-Fungible Tokens).

Investing in Blockchain right now, if you have a long enough time horizon, is probably a good idea. There are so many companies, that IBM built a Blockchain. If I was dabbling and I didn’t want to get left behind which is where most people are, I wouldn’t go buy Crypto personally unless you’re prepared for the vicissitudes of what is Crypto right now.

You can find great companies – IBM, Microsoft, etc., that are building in Web3 on the Blockchain, and so on. It will get reflected in their stock price and you don’t have to deal with all the volatility that comes with Crypto. That’s the first.

Speaking to those who feel like, “I’m going to get left behind” they’re leaving their comfort zone to go buy Crypto. If you buy Crypto because you have FoMo (Fear of missing out), and you have not experienced 70 percent Drawdowns before, don’t buy Crypto. Find a company, like an ETF (Exchange-Traded Fund) or something more familiar. Investing in companies that are tinkering with the Blockchain as a tech is a good move.

Those are the same companies that are tinkering in AI and they’re probably going to combine the two to do some cool stuff. It won’t be as sexy or fun as Dogecoin, going to Gazillion X, but it would get reflected in their stock price. People would be happy with it.

On the Crypto side, NFTs right now are great. Inherently, there’s no value to NFTs outside of their sub-utility, the providence, and the royalties. NFTs – I would look at it like, “Do I believe in this project?” Fundamentally, there’s no value identity unless it’s subjective.

Cryptocurrencies, that’s the interesting thing to me because when a lot of people look at Crypto, they look at it like they would invest in Apple. What’s interesting is that, when you invest in Apple, you’re not investing in Apple thinking that a whole bunch of other people are going to buy Apple necessarily, because there’s an invisible third party.

The people standing outside an Apple store to buy an iPhone are participating in the market, but they’re not buying and selling stock. Crypto doesn’t have that third party participating yet like equities do, or even commodities.

Commodities somewhere, the rice is getting delivered, cooked, and eaten. There’s no third-party participant yet, which makes it highly speculative. Everybody knows that. The other thing about Crypto, for the most part, the commodities market exists for Bona fide hedgers – for people who want to stay in business.

The readers are probably familiar with that. The Commodity Market exists for Bona fide hedgers, they allow speculators to participate so there’s sufficient liquidity. Equities exist so you can invest in companies. You could have a piece of these performing companies. Crypto is different in the sense that there’s no equivalent to Bona fide hedgers and not all Crypto assets are built or designed to be investments. They ended up sometimes as the utility.

That’s when investors have a hard time. It’s like, “I bought this coin and it didn’t go up.” Well, it’s not designed to go up or down. It has a utility. The reason you would buy this Asset is to perform the function that it does. This is why most people get wrecked (for lack of a better term), is because they look for assets that are going up or down.

Unlike any other market that I’ve seen, each of these Crypto assets has a different utility within an ecosystem that you probably don’t understand yet. If get into Crypto, the easiest thing to do is study Bitcoin. It’s been studied for thirteen years and people understand it.

Elon Musk, and Michael Saylor, bought it. If you start Ethereum, you can learn a lot about it. It’s mostly publicly available. Anything smaller than that, if you don’t understand the utility of it, I’m not sure if it’s a great idea to buy it.

I know that makes sense. Do you think it’s too late to get into the game for people? Let’s say someone is not technically inclined to go deep in this Asset class, but wants some exposure to it. Is there any kind of general thoughts about that? Maybe Bitcoin, Ether, and some kind of percentage.

Yes. This is only an opinion and not a financial advice. All those other disclaimers again. I do have a thought on it, I was too young, but the dot com (.com) bubble was there. You could make sound arguments for a lot of those companies, I’m sure. Most of them don’t exist anymore.

That’s where we’re at with Crypto, you could look at the Top 20 projects and I’d be willing to bet that five of them still exist ten years from now. That’s my disclaimer. Fundamentally, this is what I believe now. There was a time when I would have told you that there’s no way that any search engine ever takes over Ask Jeeves. Who uses Ask Jeeves anymore? Things are changing quickly.

Bitcoin is likely the safest bet and you can go deep dive into it all you want. There’s a lot of great information out there. In my opinion, the question is this, is Bitcoin going away? Yes or no? I don’t want to influence anybody’s answer. That’s the first one. My opinion is, no. Look at it, it’s not going away.

There can only ever be 21 million Bitcoins, which means not even every millionaire in the US (United States) could have a Bitcoin. That alone tells me it’s a sound investment. Just know that it’s not going away and it’s already worth sixty grand. I would assume there’s going to be a supply-demand issue. The tech doesn’t matter to me. If we’re talking about investments, it doesn’t matter.

To accelerate your path to wealth, as defined by you, take time to gut-check yourself on what truly matters.

Bitcoin is a sound investment. If you have a long enough time preference because regulation and all this stuff is going to be volatile. For most things right now, Bitcoin has no utility outside, it’s like having gold. There’s not much you could do with it. It’s a slow network.

Ethereum, if you look at all the projects – Bored Ape Yacht Club, all these NFTs, they’re all built on Ethereum. At this point, if any projects in Crypto win other than Bitcoin, Ethereum wins. For that reason alone, I would have Ethereum. I’d take a bet on Ethereum. If I was going to bet on Crypto, I would bet on Bitcoin and Ethereum.

Whatever reason you have as an individual, great. But fundamentally, I don’t think there’s much of a benefit in diversifying beyond those two if you’re just starting. The other thing you have to worry about is tracking it all. Bitcoin and Ethereum are very easy to track. You start getting smaller caps, you start losing track of how to check the price, where it’s at, how to sell it, how to buy it – all that stuff.

Nic, we talked about the speculative nature of Crypto, and we’ve talked about the utility of Crypto, but how about the perspective of people thinking about it as an Asset class that’s a Hedge against the dollar?

That’s a great question. First of all, I have partners who are formally trained in all this stuff, I am not. For all the investors listening, I apologize because I’m going to use layman’s terms. Hedge against the dollar – here is the issue I have with that concept. Conceptually, I understand. But here’s the issue I have with people that want to have that conversation. Most of them cannot formulate a good argument. I’m sure there are plenty of good arguments.

When you buy Bitcoin, how do you measure whether or not it is a good investment? How many dollars it’s worth? We want to hedge against the dollar and you believe that, but if your behavior and your reaction goes, “I bought Bitcoin and now it’s down.” So you wanted more US dollars to hedge against the dollar?

How’s that different than any other investment? If we measure our Bitcoin value in Bitcoin, I have 0.3 Bitcoin, and then tomorrow I still have 0.3 Bitcoin. 0.3 Bitcoin will get me more cheeseburgers today than it would yesterday or the same dollar.

Until you start doing that kind of math and having that conversation, I don’t think anybody’s hedging against inflation or the dollar being devalued because they’re just trying to acquire more dollars, based on my observation. It’s like any other investment. It’s a hedge against the dollar weakening in the sense that you’re hoping to have more dollars. But you can’t go into Chevron and buy gas with Bitcoin. For now, in time, it will prove to be a good hedge.

It’s similar to how right oil has always been pegged to the US dollar as well.

If you’re looking at the investment right now, I’m only saying this so people can align their strategy with their reality. People are like, “I hate the US dollar. Get rid of that trash.” Then they buy Bitcoin and they go, “My Bitcoin is worth less US dollars.” Those two things don’t live well together.

You either hate the dollar, or you love it and you want more of it. It’s like these beliefs and actions that are opposed that cause a lot like, how do you have a sound investment strategy when your beliefs are opposed to one another?

For the readers out there, the data that I have collected so far on Ultra-High Net Worth and Family Offices has been 1% to 3% on average as part of their portfolio allocation into Cryptocurrency. Just as a data point.

It’s great. I do think that will go up. This is why everybody, when you mentioned that you think we’re late, we’re all still early because regulatory clarity will increase. High net-worth people will invest way more when they have clarity on the legal ramifications of investing more.

Excellent. Nic, if you could give just one piece of advice to the listeners about how they could accelerate their wealth trajectory, what would it be?

Make a distinction between, speed – going fast, and velocity. Adding the vector component, go fast in the right direction. To accelerate your path to wealth as defined by you, take time and gut-check yourself on what matters to you.

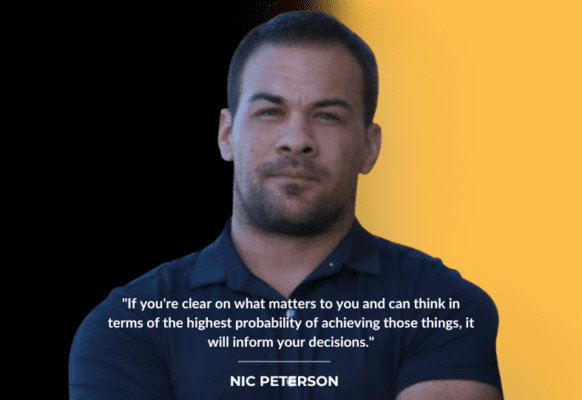

What are the most important things? That will help many people discern the right investment for them. If you’re super clear on what matters to you and you can think in terms of what’s the highest probability that you get the things that matter to you, it’ll start to inform some of those decisions.

If you can learn through the lens of biology, complex systems start to make more sense.

Awesome. So many great takeaways. I appreciate the insights, Nic. If people want to learn more about what you’re doing with you, Wolf Den, or your companies, what’s the best place?

The best place is probably just to start with the book. If you go to bumpersbook.com, it’ll take you straight to Amazon. The reason I send people there is because one, I don’t have anything to sell to people. Two, you read Bumpers, it’s super short. In my experience, it’s either self-evident and you get it, or it’s not your thing. It’s the best filter I have. Read the book. If you like it, you’ll figure out how to find the rest of my stuff. If not, it’s cool. It’s 45 minutes of your day, now you know.

Awesome. I’d like to throw something else out. If you guys could do Nic a huge favor to thank him for his time today, I noticed that you’ve got about 85 reviews on Amazon and as I understand that the algorithm is about a hundred reviews, it’s going to move up into the suggested category more.

If you guys could go in when you have a chance to download Bumpers and read it, please give Nic a review on that. If he gets fifteen more reviews, we’ll be across. I’m going to do one myself, hopefully we’ll cross that threshold, and get a lot of value out of it as well.

That’s great. I didn’t know that but thank you.

You bet. Nic, thanks again. I appreciate the dialogue. It helps people challenge some of the conventional thinking that we’re all subjected to and think outside of the box on what wealth means to you, how you allocate capital, and what’s important.

It was fun. I haven’t talked about investing since, it’s probably been a year. It’s good to drum up some of this stuff.

Awesome. Nic, thanks again. I appreciate it.

Likewise.

Important Links

Connect with Nic Peterson

Connect with Pantheon Investments

Books Mentioned

R3 by Nic Peterson – FREE Resources at The Guardian Academy

People

Further Resources

Your 10-Step Actionable Checklist From This Episode

✅ Identify and articulate your primary objectives, whether in wealth, business, or personal life. Define specific, measurable outcomes and timelines.

✅ Create safety measures to prevent significant losses. Establish boundaries and protocols that help you avoid high-risk decisions and mitigate potential damage.

✅ Recognize and reward yourself for maintaining good habits and avoiding negative behaviors. Reinforce actions that contribute to achieving your objectives and minimizing setbacks.

✅ Determine the most important financial goal to achieve first. Quantify this goal and set a specific timeline for achievement.

✅ Balance your portfolio with high-upside investments and reliable, low-risk ones.

✅ Fund one priority at a time fully before moving on to the next. Avoid spreading resources thinly across multiple priorities simultaneously.

✅ Focus on understanding Bitcoin and Ethereum, the two leading cryptocurrencies. Learn about their utilities, histories, and market performances.

✅ Stay informed about regulatory developments in the cryptocurrency market, as these can significantly impact investment strategies and market stability.

✅ Read Bumpers by Nic Peterson to gain insights into effective investment strategies and decision-making. You can purchase the book from Amazon and leave a review to help it reach a broader audience.

✅ Connect with Nic Peterson on his website and LinkedIn for more insights and guidance. Engaging with thought leaders can provide valuable perspectives and enhance your investment knowledge.

About Nic Peterson

Nic Peterson is the co-founder of Mastery Mode, helping business owners build systems to increase profits and free time. He has founded several successful companies, including Certainty U, the Certainty App, Relentless Performance, and Trevor Kashey Nutrition. A lifelong learner, Nic shares his knowledge to help extraordinary people achieve remarkable things. If you have a cash flow-positive business, reach out to him at CertaintyU.com. For those just starting, explore the free resources at the Guardian Academy.

Nic Peterson is the co-founder of Mastery Mode, helping business owners build systems to increase profits and free time. He has founded several successful companies, including Certainty U, the Certainty App, Relentless Performance, and Trevor Kashey Nutrition. A lifelong learner, Nic shares his knowledge to help extraordinary people achieve remarkable things. If you have a cash flow-positive business, reach out to him at CertaintyU.com. For those just starting, explore the free resources at the Guardian Academy.