Listen Here

![]()

![]()

![]()

Today, we had the pleasure of hosting Jim Sheils, a distinguished guest with a multifaceted career spanning real estate investment and family education. Jim, a partner at Southern Impression Homes, highlighted his expertise and specialization in constructing rental portfolios for both individual investors and institutional buyers in Florida’s burgeoning markets.

Today, we had the pleasure of hosting Jim Sheils, a distinguished guest with a multifaceted career spanning real estate investment and family education. Jim, a partner at Southern Impression Homes, highlighted his expertise and specialization in constructing rental portfolios for both individual investors and institutional buyers in Florida’s burgeoning markets.

With a focus on new construction and low-density properties like single-family homes, duplexes, and quads, Southern Impression Homes offers turnkey solutions with property management services in place, ensuring maximum returns for its clients.

In this episode, Jim delved into the synergy between his dual passions for real estate and family education, emphasizing the importance of holistic wealth management and the profound impact that strong family ties have on long-term prosperity.

He also shared a wealth of actionable advice and inspiring anecdotes, making this episode a must-listen for anyone aspiring to achieve true wealth and fulfillment in all aspects of life. Tune in now to gain exclusive access to Jim Sheils’ wealth-building wisdom and transformative insights!

In This Episode

-

Jim’s career spanning real estate investment and family education

-

Creating value through strategic renovations and management

-

His commitment to empowering others in achieving financial freedom through “Passive Income Playbook”

-

Striving for holistic wealth management, encompassing financial, emotional, and relational aspects

Welcome to today’s show on Wealth Strategy Secrets. Today, we’re joined by Jim Shiels. Jim is an experienced Real Estate entrepreneur. He is also a partner at Southern Impression Homes in Florida, specializing in the Build-to-Rent sector offering new low-density rental homes.

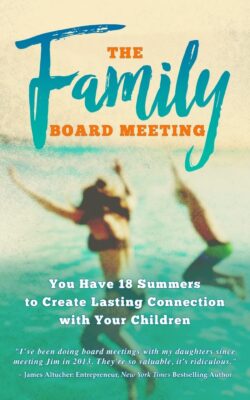

Jim is also the co-founder of 18 Summers, targeting work-life balance for business leaders. He co-authored with his wife, Jamie Shiels, one of the bestselling books, The Family Board Meeting.

I am excited to dive into the discussion here with Jim. You’re going to learn a ton today, especially how to use Build-to-Rent in your portfolio and potentially even use this as a strategy for becoming a Real estate professional, that potentially your spouse or yourself could qualify for managing a portfolio of Build-to-Rent homes. I hope you enjoy it. I appreciate having you here on the show Jim, and I’m looking forward to the discussion.

Thank you for having me, Dave. It’s good to be here.

Cool. Why don’t you help the audience get to know you? Let’s talk about your background. How did you get into Real estate and Build to Rent in the first place?

My Real estate journey started almost 25 years ago. I had been looking for something to do on my own, branch out on my own, and become an entrepreneur. I kept coming back to Real estate. I liked the quote at the time which was, “Eight out of ten millionaires made their money in Real estate”, which was appealing to me. I liked the tangibility. Like everyone else, I started with that first house at 432 North M Street, doing old rehabs, fixing them, renting them, or reselling them.

I did well with that and then grew into a bulk foreclosure model where I was buying bulk foreclosures about five or six years into my career. That went well, especially after 2008 and 2009. I moved from California to Florida and that was a good time to be in the foreclosure game with all the 2008 meltdown. But, by about 2014, we were seeing a lot of the deals that I focused on going away.

My building partner now came to me, we had done some deals together, and said, “What if we build our investment property for ourselves and investors instead of trying to find old houses to renovate?” And that was the inception. That was where I hit stride. Real estate has bought back my time and given me financial space I never thought I’d have in my life. But the stride hit about a decade ago when I went into Build to Rent.

Today, we work with nearly 1,000 investors, we’ve done over 8,000 units, created over 180 million in equity for our investors, and 44 million in recurring revenue. We have almost a billion dollars under Asset management. We grow our rental portfolios with our investors in high-growth markets in Florida, not Miami, not Tampa, not Orlando.

Those areas are out of whack when it comes to cash flow and what we like for the affordability index. But a lot of second-tier markets in Florida are where we’re focused right now. We have about 5,000 lots that we’re building out a combination of single-family duplexes and quads.

Fascinating. What did you do before real estate?

It’s not what real estate is, but what it provides. Most people view it as a means to buy back their time and enhance their family life.

I was in Corporate America for about two years. That’s all I could last. And I was in pharmaceutical, I made it that long. I remember I was sitting in a cubicle doing a pamphlet for irregular bowel syndrome for a pharmaceutical company. It was almost worse than it sounds. I didn’t last long in Corporate America. I quit that second job after a big promotion, after my first year there, and went the entrepreneurial route.

It’s always interesting to hear what that light bulb moment was for people that made them take this leap into getting into passive income, investing alternatively right from what Wall Street would have you believe is the only way to invest.

Interestingly, I was going to ask, how does your model work? Typically in Build to Rent, we’ve seen a lot of players on the smaller side. Most of our audience is interested in more passive investing because they’re looking to scale their portfolios as well as their time. How does your model work?

The foundation of our model is new construction. I’ve done a few thousand of the old fixer-uppers and now several thousand of the new construction. First and foremost, our model is only new construction. We don’t offer fixer-uppers anymore. Most of our investors are high net worth, wealthy people who want to buy back their time. They’re not looking to create a second job or have too much involvement. They want to be in real estate, but I have a lot of the heavy lifting handled for them.

What we do is try to bring in all of the unknowns – needed questions, and we answer them. First and foremost, where do you build? Where is there rental demand? What type of property? Where are we going to have the best returns, especially even in high-growth markets? How do we finance them? One of the most important things we do is when you do a property with us, you don’t need a construction loan. We’re on what’s called a ‘continual build’ cycle.

We have zero bank debt. We are financed by a parent company that owns part of our company now. A 330-year-old company out of Japan. We have no restrictions with banks on our building.

We do a continual build – which means a lot of people who buy a Bill to Rent property might sign up for it, and they have to wait a year or 14 months. Since we’re on a continual build, we have properties that are ready now. 60 days from now, or 90 days from now, we can start to build a portfolio a lot quicker.

Along with that, we’re one of the only groups I know that offer in-house financing. Right now, we’re locking in a lot of our investors on our dime at 4.75%. And if you go into a normal mortgage company right now, you’re looking at over 7% especially financing a duplex or a quad. By doing this; one of the important things as I said is scale. Most of our clients don’t buy one property. Most have sold a business or are doing well and they want to build a portfolio that they can have for generational wealth or extra income. They’re looking normally at buying about five to ten properties. We have to do that larger scale to fulfill those needs.

Two of the most important things are financing and property management. We offer property management on all our properties. For a lot of the incentives, we’ll give one to two years of free property management for those first people who buy the properties through us.

Would an investor invest in one particular unit, potentially five, or one at a time?

One property, one single family, one duplex, one quad. Our most successful investors usually own a combination of all of them. They put it all into the recipe. They all have their extra perks, I believe. I own single families, duplexes, and quads. They all are residential in theme, which is a good thing, and which I can go over. But they usually buy a combination.

What are you seeing for the average return profile for these units?

You’re looking at a five to eight cap on one of our properties.

From the cash flow perspective, what would an investor receive monthly dividends based on this, obviously for the rent that’s coming?

You can buy a property for 50 cents on the dollar, but without proper management in place, you could still lose money

Our goal is always cash flow off the bat. I know a lot of people are saying today, “You can’t cash flow new construction right off the bat. You have to have a negative cash flow.” That’s not true. When we’re building out to the scale, we are and have gotten prices down and able to offer this low-interest financing. We’re getting people sometimes as high as 10% or 11% cash on cash return right out of the gates. Our Property counselors go through all of our different performances. People can see exactly where we’re coming up with those numbers.

Are there any tax breaks that investors can take advantage of?

Everyone’s tax situation is different, but for most of the people we work with, owning a rental property is a good way to hedge taxes. I know it’s been helpful for me and my partner. There are tax incentives to owning your property as opposed to, let’s say, investing in a fund or syndication. Those can be great, and I invest in those as well. But the ownership has some real taxes and incentives that our people enjoy.

Are you seeing investors doing Cost Segregation on single families?

Some do Cost Segregation on some of the bigger ones. There is great depreciation. That first year that you own the property, normally the property tax is only taxed as land. That is a huge saving in that first annual tax bill. That’s a few of the incentives tax-wise.

How about from a property management perspective? You mentioned that sometimes, you offer some Property Management on the front end. Is that an ala carte type service, or how does that work?

We started management before we went into Build to Rent. How this started – my building partner’s father owned a large property management company. I had a lot of properties that I moved over to them to manage. I didn’t like managing my properties. I had hired and fired four property managers in the northeast, Jacksonville area. They took them over and did a good job. We knew that if we were going to do this model correctly, we had to have management in every market before we even started building.

Management is something we’ve done even longer than building. That is key. My mentor used to say, “You can buy a property for 50 cents on the dollar, but if you don’t have management in place, you could still lose money.” We always try to provide the management with incentives. Being the builder and the property manager is a rare thing. First off, we can offer those types of incentives. We’re saying, “We’ll squeeze our numbers down for the first year in management” because it’s there more to please the client than to please us.

Because management is not the funniest part of the game, but it’s something important. We can offer one to two years of free monthly management, which is great – bottom line cash flow, and takes a lot of the worries off. People find a new construction home, that’s one thing. But if they can’t find management, they put their money at risk, and we knew we had to take that out of the equation.

If an investor were to approach you and say, “Invest in one or more of these properties.” Are there also ways to drive the appreciation in that? Typically, with multifamily properties – you’re moving in, adding a pet park, doing value additions such as installing low-flow toilets and boosting revenue. Are there any Build-to-Rent properties that you know of where you can increase appreciation in these units?

It’s been interesting on the force appreciation. Picking the right market is key. We’re able to get reports from the municipalities in different areas of Florida. When they’re behind on needed rental inventory, right there is an absolute north star to some potential appreciation.

If we’re behind on that needed rental inventory and we’re building it, we know that we have wind in our back. Another thing that’s happened, which I’m sure you’ve heard about has been interesting because it’s never been our focus, but we’re getting buyers from it, it’s helping sales comparables, and they’re already going up, which we didn’t expect.

It’s not the size of your portfolio that matters; it’s the things you care about in life, like your health and your family.

We expected 2024 to be more of a flat market. That’s what everyone was saying. As we go into this election year, rates are going to start sliding down. We’re already seeing that it happens almost every time there’s an election, but there’s still a stagnant. We’ve seen some growth, especially in the duplex and quads.

What happened at the end of November was, the FHA reduced the down payment. I don’t know if you’ve seen that, where the down payment used to be; but if you’re a first-time home buyer going in to buy a duplex, you had to put 25% down. The FHA, which is the government-backed, first-time home buyers loan is now 5% to buy a quad, a duplex, or a triplex. We don’t build triplexes, but two, three, or four-unit, all residential. That’s a big difference for someone to be able to come up with the down payment at 5% as opposed to 25%.

We’re seeing some forced appreciation as more buyers enter the market for inventory that’s not always readily available, such as duplexes and quads. We’re one of the only builders I know that build these. They take a little more to get approved and go through. We’re seeing some forced appreciation from that one guideline rule with the FHA.

I hadn’t heard that. I’ve got some 20-year-olds who are looking at first-time homes and the market is high for those first-time home builders. That’s interesting if they can put only 5% down.

Something to look at. My 20-year-old son is looking at it as well – a duplex with us because he can almost live for free and the down payment is 3% to 5% as opposed to 25%.

That’s huge. How about from an investment perspective? You have a lot of investors coming into these deals. You talked about you providing financing, which is unique. Let’s say, I came in, I wanted to buy one of these properties. I want to put in my investment entity. Can I coordinate that financing with you? Or how does that work?

One of the jobs of our property counselors – some of them have been with me for 14 years, do their deals, they understand. The first thing we want to do is make sure we’re a match as we’re not a match for everybody. People say, “We have no time.” I say, “We’re probably not for you. Put it into a funder syndication.” I always like to keep those guardrails up for at least two hours a month. You might only use five minutes that month to check your statement, rents have come in, and no charge is great.

I always say that you should have about two hours a month readily available to be able to manage a small rental portfolio. If you have no time, that could be a problem. If there might be other things where you aren’t comfortable owning properties or having tenants, then we’re not for you. But the people we’re for, once we figure that out, we try to pick the right properties based on what your goals are.

Although we invest in building similar fundamental markets, there’s always a variance, and we try to match them up with that. Financing is one of the key elements that 99% of people use with us, because of the rate. That is the absolute starting point of where we try to get them off on the right foot. Can you qualify? To start a portfolio with us, you need about $80,000. That’s the starting point, to start rolling it forward.

We’ve had great case studies where if you had invested $250,000 into the S&P 5 five years ago, you would have earned about 10.4%. If you had invested $250,000 into a good Real Estate Fund, one where you wrote a check – it’s Real estate backed, you’d have earned about 13.5%.

You should have about two hours a month available to manage a small rental portfolio. If you don’t, it could be a problem.

If you had invested $250,000 like investors did and bought a small group of properties in our Jacksonville market, your annual average return would have been over 69%. This is the difference between owning properties. But as I said, if you don’t feel comfortable owning properties, if you don’t have at least two hours a month, then we try to steer you away. If you do like that, we try to set up everything that we possibly can, because of how this all started.

When we started doing this kind of organically, people would say to my partner and me, “Who do you use for mortgages? Who do you use for insurance? Who do you use for the title?” We didn’t even have any financial affiliation, nor do we on most of those things. We own our title company now, but it was, “Who do you use that’s going to get the job done?”

That’s how we formulated our team. That way, investors don’t have to figure that out on their own. Most of our people are successful. They don’t want to create a second job. They want the work done for them. They want a plan of how they can build the portfolio, and they want to be able to check in on it, but not over-micromanaging.

That makes perfect sense, Jim. One of the reasons I wanted to have you on the show – which is the real play here for us is because, in our community, people understand that time is their greatest asset, and we’re looking to scale our portfolios.

A unique play is if you’re looking to try to get a Real estate professional status or potentially have your wife or your spouse take on that duty. This is an ideal situation where you could get this small portfolio of properties. As you said, it’s minimal management. But that management of time is well worth it to be able to pick up Real estate pro status.

Absolutely. That is something you want to talk to your accountant about, but that is a favorable thing to have.

750 hours a year. But being able to go into something that is more turnkey like you have, versus trying to do everything on your own – source the property, understand the market, bid on the property, make all these assumptions against players in the market who do this every day for a living. You can get massive leverage by working with someone like Jim and his team to do that.

Yes, I agree.

Tell us about your latest book. It sounds exciting. I love the name of it, having the new moves. When I think about all of this, it’s like a chess move on the board. And you’re creating your chess board. Then what type of chess moves are you going to get you the most amount of leverage, the biggest amount of bang for your buck? Tell us more about the book.

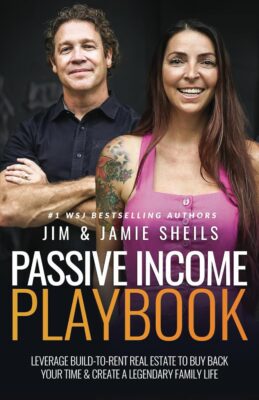

The book is called, the Passive Income Playbook, and it’s me and my wife’s journey through the Real estate. This started almost 25 years ago and includes my building partner now the mistakes we made, and the ways that we were busy, but weren’t effective; some of the misconceptions we had about having more properties all of a sudden could be your absolute end goal.

Sometimes, that could take away accomplishment and give you an extra headache. I talk about how my portfolio is much smaller in individual property numbers, but I have more cash flow or more equity than I ever have in my life. A lot of that came from the types of properties I looked for, the types of properties I invested in, and the way that I looked at long-term buy and hold. These are all an important part of the journey.

What I’m always trying to encourage people to do is – it’s not what real estate is, it’s what it provides. Most people see it as a way to buy back their time and improve their family life. We always talk about a legendary family life. With passive income, I’ve been able to do things my dad could only dream of. My dad passed away a few years ago and he struggled with money his entire life; and my mom, both of them, until I was able to retire about 12 years ago. That’s what most of our people want. They have financial resources.

Our properties can provide the space where it’s not that second or third job. We try to talk about the misconceptions of real estate, the type of real estate that will take away your time, why new construction is an interesting thing, why all the larger institutions are trying to get into it, and how we as guys can still do it. How we do it when our family comes along for the ride. That’s what the book is about.

It’s great that you’re sharing all those lessons because most of us out there, are all trying to learn. And this is something we weren’t taught at any of the schools that are out there. The only place you learn is by taking action and doing things, and then trying to earn from books, podcasts, and these different resources. Luckily, we have these things available to us today. But when I started on my journey, there were no resources at all, and trying to get access was hard.

Very few.

I like that. Then your other book, I love your focus on family, which is important to us as well. We talk about having a Holistic Wealth Strategy, because that’s what it’s all about. It’s not the size of your portfolio. It’s the things that you care about in life, your health, and your family. Tell us about the book that you wrote with your wife, The Family Board Meeting.

The Family Board Meeting is not something I ever planned on writing. I thought it was too simplistic. I shared it at a few mastermind groups and people said, “You have to write a book on this.” My wife and I did begrudgingly. Honestly, at first, it was a labor of love, but it was nice to get it out.

For the first time, it had success, sold tens of thousands of copies, and then we were invited to go with a publisher and he released our book; and re-released it at the beginning of last summer. It went to number one on the Wall Street Journal, which was a total shock to us.

There are many people who seek success in business but also want to achieve success at home.

It’s something we’re proud of, but it’s the message. Know that the message resonates – that there are a lot of people who want to be successful in business, but they also want to be successful at home. As you said, there’s not a lot of stuff out there from the early days when we had financial education, passive income strategies, and entrepreneurship. I’ve noticed the same – there’s not a lot for busy entrepreneurs, professionals, and real estate investors on how to have a good family life. Especially if that matches their personalities, their strengths, and their weaknesses.

The Family Board Meeting is about some simple principles and rhythms that we used. My wife and I have five kids; to keep a strong family life, and it resonated. We’re thrilled with that. If you haven’t read it, it’s an easy read. I’m an ADD entrepreneur, so I made it a short book.

I always joke that it gets read first. If I go to a conference and a lot of people have books there, mine always gets read first, not because it’s the best but because it’s short. But it’s got a good message to it and it’s helped a lot of families. For our family board meeting strategy, we’ve estimated about 300,000 families.

That’s amazing. Can you unpack some of the tips and key principles in the book?

Let me give you two main principles to start with. One is something I call the ‘One-to-one Principle’, which is, that you have to separate the parts to strengthen the whole. It’s an unfair advantage to have a strong family life – you have a husband or wife and three kids, you have to spend time with yourself, time with your spouse, and time with each of the individual kids.

One-on-one time is overlooked. I go into this about studies and facts that we overlook. I always joke that I grew up in an Irish Catholic family, which means you have 4,000 cousins and big gatherings, and those are great.

It’s one-on-one time that helps deepen the relationship, that gets you under the surface, where bigger conversations can get out, where your spouse or your child feels extremely important to you, which sometimes when you’re moving fast, they can misinterpret. Ask yourself the question, for everyone listening, “Do I spend scheduled one-on-one time with my spouse, with my children?” I have an almost immovable date night every week with my wife, even with five kids, ranging from 2 to 20. Non-negotiable. That’s been a key to our marriage. I spend a day, a quarter with each one of my children one-on-one, they plan the day, and we go all in. It’s been some of the most groundbreaking pieces of our relationship that occurred on that one day. That is a starting point – the one-to-one.

One-on-one time deepens relationships, allowing for meaningful conversations and making your spouse or child feel truly valued, especially when life’s pace might otherwise lead to misunderstandings.

Something else that I would challenge people on – a principle I go into, is what I call ‘Intermittent Tech Fasting’. We’ve all heard of intermittent fasting if you’re into health, I’ve read that it helps weight maintenance, muscle tone, and organ revitalization. When you’re doing intermittent fasting, you’re not giving up eating, you’re saying, “I’m only going to eat between this time and this time.” What I’ve found with technology; and there’s a lot of study behind this. I’m not saying to get rid of it.

You and I wouldn’t be having this great conversation today from Sarasota to Costa Rica. However, you have to have times of complete and total unavailability. Because we’re not as multi-tasked ability as we think we are. It gets in the way. It’s an insult if you are pulling that out. When I’m on that date with my wife every week, my phone is not invited. When I take these one-on-one days with each of my kids each quarter, my phone is not allowed. Neither is theirs, but I set the tone.

You start to feel until you pull it out of the diet, where your phone or your laptop is always there. Until you pull it out and spend a couple of hours without it, you don’t realize until you’re doing it, how often you’re doing that grab, how often it’s interrupting you. I’ve worked with thousands of families. I can’t tell you how many teens have said in retrospect they were about to open up to their parents about something. They had something really heavy on them; I’m talking about the tough stuff.

We don’t want our kids to go through that their parents seem too busy. They’re on the phone, they’re getting a text, an email, or a useless Facebook thread. These periods of intermittent tech fasting make you unavailable to the outside world, allowing you to focus solely on what’s right in front of you. You couple that with one-on-one and do that on a nice schedule. It’s not going to get you all the way there, but it’s going to do you a lot of good and get you a farm.

I love that, Jim. We’re living in this world of evolutionary mismatch because when we started on this planet, we did not have all these technological conveniences that we do today. It’s taking its toll on us as a civilization. It’s a death by a thousand cuts. That’s why we’re having all these increased rates of the top diseases – cancer, you name it, all these things are building up. But I love your concept around the one-on-one because it fosters that deeper connection.

If you carve out time for individual connections, you’ll be stronger together as a group.

As you say, it’s easy to have a surface-level discussion with family members such as, “Hey, how was your day?” “That was good.” “Do you go into the game?” “I’ve got you.” Most of the time, we find ourselves talking about logistics. You’ve got like, “Are you taking care of the dog? Are you coming here? How are you going to get to the airport?” All of these kind of basic things. We’re not serving ourselves well because we have the opportunity to have these deeper connections.

My kids are now in their 20s. What I find in this challenging chapter is they’ve all flown the nest. How do you still create that overall family bond, that connection, where everyone is at different places, totally independent, and doing their things? I like that if you can carve out the time to have individual connections, then you’re stronger together as a group.

What I found for friends whose children are in their 20s; when I first wrote this book years ago, I had a friend who owned a marketing company – a busy guy and had seven children. I think the youngest one was 22. He said, “I’m not going to be able to have a half day. They’re all over the country, a half day every quarter. I’m setting myself up for a kill to their schedules.”

What he’s done for eight or nine years now, one day a year he plans a special day with each of those seven kids. The youngest one now is 24 or 25. One day a year, and the year after. Of course, they have time in between and other things, but that’s their day – a full day. Seven days a year, he’s going somewhere, wherever it has to be to have a full day with each one of their kids, doing something they want to do fun, with no phone distraction.

Where do you think you’ll be? I look back, I wish I had that with my father from 22 to 47, to when he passed away when I was 47. I didn’t get that. Even if you get one day a year, without the fun, without the distraction, one-on-one, enjoying each other, creating the space for maybe some deeper conversation or laughs and again, full focus – where could you be? That’s why I always encourage people. It is a game-changer.

That’s powerful. You’re building up those meaningful experiences year after year. We’ve been working on a family retreat in our family where everyone gets together and we can focus on our family constitution – what’s important to us, and then try to create those new bonding type of experiences, versus the typical get-together for Thanksgiving which is always chaotic for many reasons.

I love it. That’s a lot of the most successful families I’ve met. Specifically, how do we make the most of our wealth to take holidays and enjoy life to the fullest? Of course, there are holidays, but they do have one vacation adventure a year. They go somewhere and do something fun.

All the family, everyone comes and it’s a great get-together time. It is a reunification and then they might bring in as we do – like you said – some light learning, where they’re still learning together. They’re in a cool place enjoying that light learning, but they get to look forward to that every year as a group.

There are holidays and other things, but this vacation adventure is on their terms, on their schedule, and what everyone decides. My wife and I planned our goal to do that for the next 50 years if I can, or 60 years with my kids. Every year, we want to have one big adventure, even as they go off and get married, that’s going to be our annual gift.

Periods of intermittent tech fasting make you unavailable to the outside world, allowing you to focus solely on what’s right in front of you.

That’s awesome, Jim. I love and I appreciate you shared that with the audience because that’s powerful. As you talked about, we’re focused on wealth building and we talk about real estate and all of these passive income. It’s the outcome that we’re looking for. Having more qualitative time and being with our families. I appreciate that wisdom. If you could give one piece of advice about how they could accelerate their wealth trajectory, what would it be?

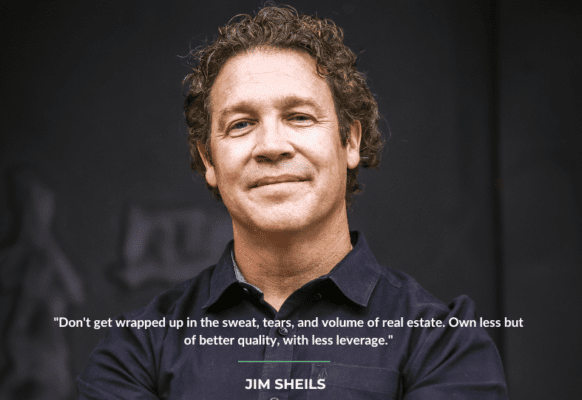

Don’t get wrapped up in tons of sweat, tears, and volume in real estate. Own less of better quality, with less leverage. That’s it. If I could go back, I would have owned less property, better quality, and less leverage. When you’re in that position, you can do well. The real estate serves you, instead of the other way around. The advice I give to all my friends and family is that if we’re getting involved and considering it, especially for those who have worked hard, built some net worth, and achieved some success.

We know we’ve got to be more involved in real estate. But I’ll say, “Great. Don’t worry about getting into the 100 Property Club.” I did that and passed it. It’s about effectiveness. It’s about the net numbers, the performance. Own less, better quality, less leverage. Grow it that way, and you can be in great shape.

Awesome. Great words and wisdom, Jim. I appreciate that. If people want to reach out and learn more about your Build to Rent or check out your books, what is the best place?

You can find The Family Board Meeting on Amazon, Barnes & Noble – anywhere books are sold. For the new one, the Passive Income Playbook – if you’re looking to grow your real estate portfolio and are interested in Build to Rent, it’s a great book, with a lot of case studies with successful clients, and our journey. You can go to jjplaybook.com and we’re offering a free digital copy there if you’d like that. That was the number one seller as well.

I appreciate your time today, Jim. Thanks for coming on.

No, it was great to be here, Dave. Thank you for having me.

Important Links

Connect with Jim Sheils

Connect with Pantheon Investments

Books

Further Resources

Your 10-Step Actionable Checklist From This Episode

✅ Begin your real estate journey by investing in your first property, whether through old rehabs, rentals, or resales.

✅ Prioritize new construction properties to avoid the challenges of fixer-uppers and cater to high-net-worth investors who value time efficiency.

✅ Work with your accountant to identify tax benefits, including cost segregation, depreciation, and favorable first-year tax treatments.

✅ Engage with property management services to ensure your investments are well-managed, allowing you to focus on scaling your portfolio.

✅ Identify markets with rental inventory shortages or favorable FHA guidelines to drive appreciation in your Build-to-Rent properties.

✅ Prioritize owning fewer, higher-quality properties with less leverage to maximize effectiveness and reduce stress.

✅ View real estate as a means to improve your family life and buy back time, rather than just accumulating properties.

✅ Implement periods of complete unavailability from technology during family time to enhance focus and presence with loved ones.

✅ Make one-on-one time with each family member a non-negotiable part of your routine, ensuring everyone feels valued and important.

✅ Utilize available books, podcasts, and other resources to continue learning and applying strategies for building wealth and improving family life. Consider reading The Family Board Meeting and the Passive Income Playbook for further insights.

About Jim Sheils

Jim Sheils is a partner at Southern Impression Homes, specializing in Build-to-Rent properties in Florida’s high-growth markets, with over 2,000 rehabs completed and a successful history in real estate investment. After merging his company, Jax Wealth Investments, with Southern Impression Homes in 2022, Jim expanded his focus on rental portfolios. He is also the co-founder of 18 Summers, where he and his wife Jamie, #1 Wall Street Journal Best-Selling Authors, help entrepreneurs strengthen family relationships through keynotes, workshops, and their “Board Meeting” strategy.

Jim Sheils is a partner at Southern Impression Homes, specializing in Build-to-Rent properties in Florida’s high-growth markets, with over 2,000 rehabs completed and a successful history in real estate investment. After merging his company, Jax Wealth Investments, with Southern Impression Homes in 2022, Jim expanded his focus on rental portfolios. He is also the co-founder of 18 Summers, where he and his wife Jamie, #1 Wall Street Journal Best-Selling Authors, help entrepreneurs strengthen family relationships through keynotes, workshops, and their “Board Meeting” strategy.